Japanese Small-Caps to Remain Resilient as Domestic Demand Recovers

The Portfolio Managers of the Hennessy Japan Small Cap Fund provide insight on inflation in Japan and the rebound in tourism. They also discuss the Japanese market, valuations, and their outlook for domestic small-cap Japanese companies.

-

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager -

Takenari Okumura, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio Manager

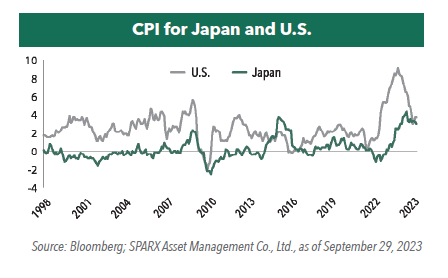

Would you please discuss inflation levels in Japan?

Japan’s consumer price index (CPI) has been above 3% over the past year, however, the Bank of Japan (BOJ) is concerned about its sustainability and has not yet changed its monetary policy. Inflation of 2% to 3% would be acceptable, but above 3% level would have negative impacts. On the contrary, a return to deflation with below 1% CPI will be the most pessimistic scenario for the economy. Given the weak yen and global inflation, we believe the likelihood of a return to deflation is small.

What sectors might be negatively affected by continued inflation in Japan? What sectors could be beneficiaries?

We believe that the materials and energy sectors would be the beneficiaries of continued inflation as they can easily pass on the costs. Also, the financial sector will likely enjoy the benefit of ending negative interest rates. On the other hand, the consumer goods sector, where price pass-through is not as easy, will face difficulty under the current inflationary pressure. It is also important to note that the negative sectors will decrease as price pass-on is gradually becoming more acceptable in Japanese society.

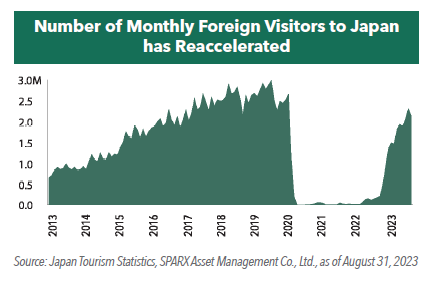

How has the rebound in tourism affected domestic companies?

With the rebound in tourism in Japan, we recognize that hotels, railroads, restaurants, department stores, and other high-end consumer goods are performing well. Inbound demand is accelerating inflation, which is positive for the overall economy. Although over-tourism has become a concern to some extent, we believe there are more positives than negatives on the back of the diversification of travel destinations and the increase in accommodations.

What drivers will continue moving the Japanese market higher?

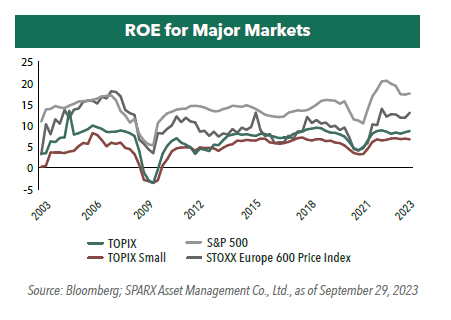

The synergy between the expansion of corporate earnings and valuations is driving the market against a backdrop of improving corporate profitability and increasing sales led by cost reductions over the past decade. In addition, Return on Equity (ROE) and valuation are also improving supported by better awareness around corporate governance.

Would you please discuss how the Fund’s holdings have been affected by the depreciation of the Japanese yen?

The Fund has a large number of manufacturing companies which can benefit from the weaker yen. However, as their sales have not yet fully recovered, their performance has not yet improved, but we believe manufacturing companies will benefit from Japanese yen depreciation in the near future. For domestic consumption-related companies, higher import prices are a disadvantage, but we believe the disadvantage will be small as they have been able to pass on the cost to their customers.

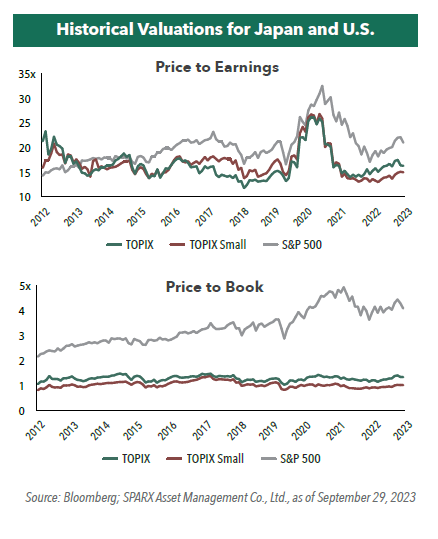

Would you please discuss current valuations vs. historical measures?

Japanese companies appear significantly undervalued with a price to earnings (P/E) of 15x and a price to book (P/B) of 1.5x for the Tokyo Stock Price Index (TOPIX). Regarding small-cap companies, they are more undervalued with a P/E of 13x and P/B of 1.2x. In addition, we believe that future earnings growth is likely to be high, which will increase the sense of undervaluation. What’s more, the Tokyo Stock Exchange is increasing its guidance for improvement to companies with P/B ratios below 1x, and we believe that small-cap stocks, of which about 30% are under 1x P/B ratios, have high upside potential.

Would you please discuss notable portfolio changes made in 2023?

Although we did not change our portfolio significantly, we initiated investment in companies with P/B ratios below 1x because of their attractive valuations and the anticipation of economic recovery. We also made a new investment in the retail sector as we believe that the share of retailers with strong price competitiveness will increase as inflation continues to rise.

What is your outlook for domestic small-cap Japanese companies as we enter 2024?

It is true that the Japanese stock market is facing heightened downside risks due to rising geopolitical risks and uncertainty over the Chinese economy. However, we believe the Japanese market will remain resilient with a continued recovery in the domestic demand economy regardless of overseas conditions.

As the Japanese yen continues to depreciate, Japan’s prices and wages are becoming increasingly inexpensive. We believe that Japan’s wages and prices will increase led by growing inbound tourism demand and rising overseas wages. Moreover, Japanese stocks remain attractively valued, in our view, and this would lead to further investments from overseas investors.

Japanese small- and mid-caps continue to lag behind, and we believe that relative performance is expected to improve.

- In this article:

- Japan

- Japan Small Cap Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Japan Small Cap FundJapanese Small-Caps’ Earnings Resilience and Improving Returns on Capital

Takenari Okumura, CMAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers cover small-cap outperformance drivers, pro-growth fiscal policy, governance reform, yen volatility, portfolio repositioning, profitability and capital efficiency trends, valuation gaps, and their 2026 outlook.

-

Portfolio Perspective

Portfolio Perspective

Japan FundA Differentiated Portfolio Focused on Margin of Safety and Upside Potential

Masakazu Takeda, CFA, CMAPortfolio Manager

Masakazu Takeda, CFA, CMAPortfolio Manager Angus Lee, CFAPortfolio ManagerRead the Commentary

Angus Lee, CFAPortfolio ManagerRead the CommentaryThe Portfolio Managers summarize the significant events that drove markets over 2025 and how the Fund remains focused on quality, capital discipline, and valuation, with a clear preference for stock picking over index exposure.

-

Investment Idea

Investment IdeaCompelling Valuations in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaJapanese equities are currently trading at compelling valuation levels compared to other developed equity markets around the world and relative to their own historical averages. We believe the Japanese market deserves a closer look.