Digital Transformation of Banks

New and innovative technology is changing just about every industry, and the Financials sector is no exception. In this Sector Highlight, we examine the digital transformation trends in the banking industry and how banks are embracing technology to adapt to consumer demands and boost growth in revenue and profitability.

-

David EllisonPortfolio Manager

David EllisonPortfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Key Takeaways

- Due to increased competition from Fintech companies, consumer demand, and a desire to increase profitability, many large banks are in the process of a rapid digital transformation.

- Established banks have operating advantages over Fintech competitors due to their brand recognition, a large customer base, and extensive financial resources.

- Banks are anticipated to offer products and services that go beyond their traditional business models, including digital payments, buy now pay later programs, and cryptocurrency services.

The Changing Landscape of Traditional Banking

Many large national and regional banks have been expanding their traditional business models by embracing a digital landscape. Several drivers are associated with this transformation, including increased competition from fintech companies, consumer demand, and productivity increases that boost profitability.

Fintech Competition

Large banks are facing increased competition from pure play Fintech companies. Fintech companies’ strength lies in their technological expertise and lower operating costs. As a result, many Fintech startups have been quick to offer enhanced digital technology, pass along lower costs to the consumer, and offer more convenient features and services compared to many large banks.

Consumer Use

The pandemic had a profound effect on consumer banking behaviors and accelerated the adoption of digital technology, including contactless payments and online tools to manage their financial activities. In fact, the use of digital banking tools rose 54% from 2020 to 2021.1

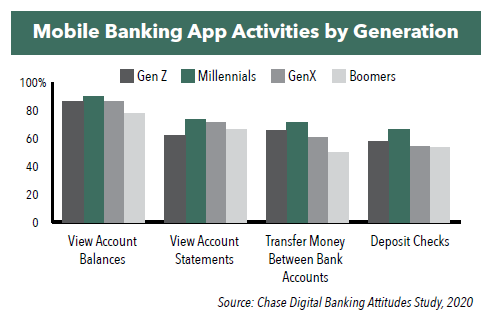

Millennials and Generation Z have been especially quick to adopt these digital tools. Among common mobile banking app activities, nearly all of Gen Z and millennials use a mobile banking app for some financial tasks such as viewing account balances, checking credit scores, and depositing checks.2

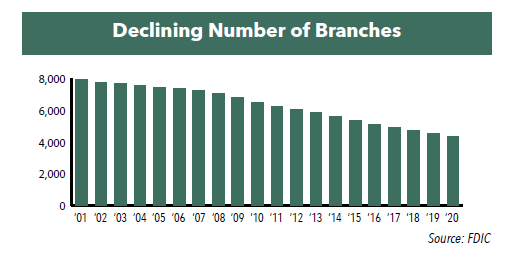

Technology disruption brings significant changes for the traditional banking industry. While there is still a need for in-person banking, fewer branches are required to service a customer base. As a result, over the past 20 years, the number of branches has declined by 45%. Due to productivity gains, U.S. banks could reduce their employee headcount by 10%, or approximately 200,000 jobs, from 2021 through 2030 in an effort to increase profitability.3

Not Only a Legacy Bank, but a Technology Company

Faced with these challenges, many large established banks have been able to build on their operating advantages, including their brand recognition, large customer base, and extensive financial resources to transform their businesses. Some banks have even referred to themselves as a technology company.

In October 2021, Bank of America CEO Brian Moynihan indicated that with about $3.5 billion a year spent on new technology-driven products and services and new code implementation, “We’re clearly a technology company.”4 Previously, in 2020, Bank of America spent approximately $8.7 billion on technology, with 40% spent on new initiatives. One such initiative was unveiling a short-term, low-cost loan program for clients to borrow up to $500 for a $5 flat fee, with repayments made in installments over a 90-day period. The company also added features to its commercial banking app, and launched Life Plan, a digital experience to track goals and understand the steps to achieve them.

Further, JPMorgan Chase plans to increase technology spending to $12 billion in 2022 as part of its “continuous business evolution” to have its team of 50,000 technologists drive innovation in tech applications.5

Over the next few years, banks are anticipated to use this increased technology budget on products and services that go beyond their traditional business models, including the following:

Expanding Digital Payments

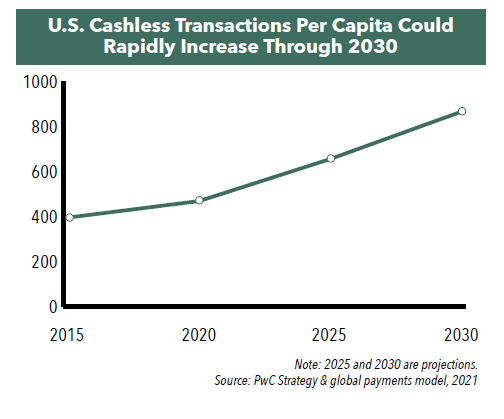

Cashless, electronic payments to send and receive money between individuals and businesses have become mainstream.

As an example, Zelle, a digital payments network, has been adopted by over 1000 banks and credit unions. The app allows you to send funds from a designated bank account. According to Zelle, consumers and businesses processed 1.8 billion payments through the Zelle Network during 2021, an increase of 49% from a year earlier.6 Total transaction volume also rose nearly 60%, totaling $490 billion. In comparison, Venmo, the digital wallet that allows individuals to pay and request money from friends, had a transaction volume of $230 billion for 2021.7

Buy Now, Pay Later Loans

Buy now pay later (BNPL) loans offer the ability for consumers to pay for purchases in installments, often without interest. These loans are popular with Millennials and Gen Z as well as those who have low credit scores. Overall, according to a Survey Monkey poll, about 20% of U.S. consumers have used a BNPL service over the 12-month period ended August 2021.8 BNPL is anticipated to grow significantly over the next few years. In fact, JPMorgan Chase estimates annual gross merchandise volume of BNPL loans could rise to $1 trillion by 2025.9

Currently, those with the largest market share have been Fintech companies Afterpay, PayPal, and Klarna. However traditional banks and other financial companies are beginning to unveil BNPL services. Credit card issuer Capital One began to test a BNPL product with a select set of merchants in 2021,10 and JPMorgan Chase has offered products similar to BNPL with its after-purchase installment payments.

Artificial Intelligence (AI) Solutions

Many banks are starting to utilize AI solutions across their business. For example, AI has been used to ensure fair access to lending and business funding opportunities and within back-office operations to track fraud detection, enhance risk management, and facilitate underwriting.

According to the IDC, a global provider of market intelligence, between 2021 and 2025, retail and banking are the two industries that are expected to spend the most on AI solutions. Of the $204 billion spent worldwide over the 5-year period, the banking industry is anticipated to make up approximately 14%.11

Cryptocurrency Offerings

Recognizing the investor demand to gain more exposure to digital assets, some banks are now offering cryptocurrency services to clients along with launching crypto trading desks. JPMorgan Chase even started its own digital currency called JPM Coin in 2019. Citibank invested in blockchain-based payments and settlements startup SETL, which facilitates the movement of cash and other assets. Morgan Stanley has backed NYDIG, which gives private wealth clients of Wells Fargo, JPMorgan Chase, and Morgan Stanley access to Bitcoin funds.

BofA acknowledged that with a $2 trillion+ market value and over 200 million users, digital assets were too big to ignore. In response, the company formed a new division focused on cryptocurrency research in 2021.

Cryptocurrency is still in its infancy and regulators are continuing to develop rules governing its use. This is a trend that will likely evolve over time and gain momentum, compelling the banking industry to expand their products and services in digital assets.

Capturing Compelling Opportunities in the Financials Sector

As the banking industry continues to make significant investments in technology, we believe digital innovations will provide banks the opportunity to capture higher market share relative to Fintech companies through increased customer services and further enhance profitability through productivity gains.

Take advantage of the ongoing digital transformation in the Financials sector with the Hennessy Large Cap Financial Fund. With an active management approach focused on bottom-up research, we seek to own a concentrated portfolio of high-quality banks and financial services companies with compelling long-term growth potential.

- In this article:

- Financials

- Large Cap Financial Fund

- Small Cap Financial Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Large Cap Financial FundSmall Cap Financial FundSolid Industry Fundamentals & Continued Consolidation

David EllisonPortfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio ManagerRead the CommentaryPortfolio Managers Dave Ellison and Ryan Kelley review 2025 bank performance, fintech-driven consolidation, attractive valuations, and their constructive 2026 outlook.

-

Portfolio Perspective

Portfolio Perspective

Large Cap Financial FundSmall Cap Financial FundSeeking Innovation in the Financials Industry

David EllisonPortfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio ManagerRead the CommentaryPortfolio Managers Dave Ellison and Ryan Kelley discuss what’s driving performance in the Hennessy Large Cap Financial Fund, how tariff increases affect banks, the interest rate environment, and the opportunities in financials.

-

Viewpoint

ViewpointNavigating the Financial Landscape in 2025

David EllisonPortfolio ManagerWatch the VideoHennessy Funds Portfolio Manager Dave Ellison discusses the key drivers behind the financial sector's strong performance in 2024, the impact of potential rate cuts and regulatory changes, and the evolving landscape of banking in 2025. He also explores the challenges and opportunities facing both large and small banks, the role of AI, and the critical risks to watch, from traditional credit concerns to transformative technological shifts.