Positive Long-Term Outlook on High Quality, Secular Growth Businesses

The Portfolio Managers of the Hennessy Focus Fund discuss the portfolio companies that represent the most relative opportunity, the effect of higher debt costs and consumer spending trends on holdings, the increased weighting in Cogent Communications, and their 2024 outlook.

-

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager -

Brian Macauley, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio Manager -

Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

With the turbulent market environment in 2023, which type of portfolio companies do you believe represent the most relative opportunity?

Within our portfolio, long duration equities, i.e., stocks that are expected to generate the bulk of their cash flow in the more distant future, underperformed over the last twelve months reflecting higher interest rates and the macroeconomic climate. When the Federal Reserve becomes confident that inflation is moving sustainably down toward its 2% goal, we believe the Federal Open Market Committee will begin to cut rates. We believe that long-duration equities will benefit the most from lower inflation and lower interest rates.

For example, two of our holdings with significant real estate exposure, Brookfield Corporation and American Tower, hold long-duration assets and are able to employ meaningful financial leverage because of the consistency of their cash flow.

The market value of the assets they hold is highly sensitive to long-term interest rates and lower interest rates would allow their assets to be financed at a lower cost. We believe both companies are poised to see significant outperformance if incoming data suggests inflation is on a path toward the Fed’s target.

In the higher interest rate environment, how will higher debt costs affect the portfolio companies?

Most of the Fund’s holdings use modest amounts of leverage. This is typically in the range of 2.0-3.0x Net Debt to EBITDA which we believe is prudent given their predictable business models and high levels of revenue visibility. This small debt load introduces lower cost debt capital into the capital structure and drives higher returns on equity while limiting the risk of a permanent loss in value. In response to the increase in rates over the last few years, we are seeing management teams take their firms’ leverage down to the bottom half of the 2.0-3.0x range to limit interest expense.

That said, at the margin incremental borrowing costs have increased, first as floating rate debt costs moved up rapidly and then more slowly as fixed debt matures and is refinanced at higher rates. Most of our businesses skew their debt to intermediate term fixed maturities, anywhere from two to seven years, so the higher cost debt is layered in over time. As this occurs over the next five years, our companies should see a modest headwind to growth in EPS as fixed maturities come due and are rolled over in a higher rate environment.

How have the latest consumer spending trends in the U.S. impacted your portfolio holdings, particularly as it relates to CarMax, American Woodmark, RH, and Hilton?

Consumer spending has held up reasonably well in 2023 considering the rise in interest rates and relatively high levels of inflation. However, consumers still appear to be prioritizing spending on “experiences” rather than “things.” We see this in some of the businesses that we own, such as Hilton, which continues to see strong demand for domestic leisure travel, and RH, which has seen a notable decline in sales of its home furnishings. We also observe that the high income consumer is faring much better than the low income consumer. We see this most acutely at CarMax, where overall unit sales are down high single digits, driven by a fairly stable middle- and upper-income buyer, and a significant decline (<50%) from consumers with household income less than $36,000.

Would you please discuss your investment case for increasing the portfolio weighting in Cogent Communications?

Cogent is a relatively new position in the Fund. We purchased our first shares in the fourth quarter of 2022, added modestly in the first quarter of 2023, and added significantly in the third quarter bringing it to about a 5% position weighting. Our investment case for Cogent is primarily based on the belief that an acquisition, announced in August last year and completed in May of this year, will enable significant value creation. However, this is a large acquisition that requires heavy expense cutting, network upgrades, and a new product introduction to deliver on its promise. Execution is key, and the transaction is not without risks. While we have confidence in management, we paced our share purchases to monitor how the initial integration and product launch are going. With the company six months into the process, we have significantly increased confidence and adjusted the position size to reflect our view.

Many American companies are moving manufacturing back to the U.S. Are any of the Fund’s holdings reviewing their supply chain or repatriating their own facilities?

Across the Fund’s 23 holdings, we can identify only two companies that are making any material changes to their supply chains and in both cases the changes are minor in the breath of their business activities.

• American Woodmark is moving the sourcing of a few kitchen/bath cabinet hardware components to Mexico from China. This has been going on for the last few years.

• RH is an upscale home-furnishings company that is slowly moving some of its furniture sourcing relationships from Vietnam and southeast Asia to more locations in the U.S. and E.U.

What is your market outlook for 2024?

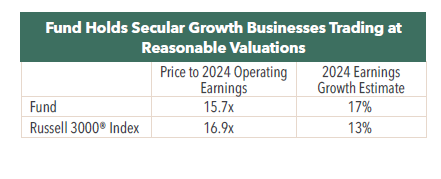

We think it is nearly impossible to accurately forecast the market over a one-year horizon on a consistent basis. We feel more comfortable providing an outlook for the next five years. Because the Fund’s holdings are predominately a collection of what we believe to be high quality, secular growth businesses trading at reasonable valuations, we continue to have a positive long-term outlook. Our expectation is that on average the Fund will own these businesses for five years or longer. Over this long-term time horizon, we expect that the Fund’s returns will likely be determined primarily by the growth in earnings power of these businesses. Our expectation is for mid-teens earnings growth for the portfolio over a five-year horizon.

- In this article:

- Domestic Equity

- Focus Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Focus FundSeeking Companies with Strong Growth at Attractive Valuations

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers rely on their strategy of owning durable, well-run businesses capable of turning adversity into opportunity and adapting to macroeconomic surprises. The following Hennessy Focus Fund Commentary recaps the 2025 market and highlights areas of opportunity ahead.

-

Portfolio Perspective

Portfolio Perspective

Focus FundFrom Rate Cuts to AI: Positioning the Portfolio for Potential Opportunity

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers discuss holdings that could potentially benefit from lower rates, tariffs, and artificial intelligence (AI). The team also provides an update on AST SpaceMobile and discusses potential opportunities in select Technology and Health Care companies.

-

Company Spotlight

Company Spotlight

Focus FundO’Reilly Automotive—Revved for Growth

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the SpotlightO’Reilly Automotive is a leader in the automotive aftermarket parts industry in the U.S. The company’s scale, unique distribution infrastructure, and customer service-oriented culture should allow it to take market share in a fragmented U.S. market for years to come.