AST SpaceMobile: Transforming How the World Connects

AST is building the first and only space-based cellular broadband network accessible directly by everyday smartphones with both commercial and government applications.1 With strategic investments from leading technology players such as AT&T, Verizon, Vodafone and Google, AST has the bold goal to provide uninterrupted broadband connectivity, everywhere.

-

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager -

Brian Macauley, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio Manager -

Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Eliminating Connectivity Gaps in Broadband

AST’s vision is to provide mobile broadband wireless coverage to existing cell phones in partnership with today’s global, mobile network operators (MNOs). Supplemental coverage from space through AST’s satellites would be a breakthrough for the wireless and satellite industries, allowing satellite delivered mobile wireless service to expand beyond niche applications we see today to broad consumer adoption.

Addressable Market

Even in 2026, billions of people around the world have no or limited mobile internet access. Among a global population of 8.2 billion, 5.8 billion unique cellular subscribers move in and out of basic and broadband wireless coverage daily, while more than 3.4 billion people are unable to access cellular broadband. Of these, 3 billion have a usage gap and 400 million have no cell coverage.

In fact, ~90% of the Earth’s surface has no cell coverage whatsoever.2 Even in covered areas, there are millions of dead zones and grey zones in existing terrestrial networks. AST plans to eliminate these gaps by providing an overlay or supplemental broadband service that mobile subscribers can opt into through their MNO’s domestic service plans—resulting in broadband coverage for the unconnected billions.

AST’s Vision

AST has announced plans to launch over 540 dual-use satellites over the next seven years designed to eliminate global connectivity gaps for commercial and government users. Four separate constellations are envisioned, engineered to serve either C-band, midband and low-band communications spectrum. The first constellation will consist of up to 248 low-band satellites orbiting between 285-329 miles above earth. Seven years in development, these low-band BlueBird satellites use a novel design, internally developed software and custom hardware that is then spliced into the wireless operators’ “core” network through an equipment partnership with Nokia. This technique allows a cell phone to see a virtual cell tower broadcasting on either their MNO partner’s existing terrestrial spectrum or later on Mobile Satellite Service (MSS) spectrum owned or leased by AST.

Worldwide Military and First Responder Opportunities

Importance of Space-Based Defense Systems

If the war in Iran has taught us anything it is that ground-based radar is vulnerable to missiles and drones guided by satellite systems. If our ground-based radars are knocked out our defensive interceptors are blind. This vulnerability is being rapidly incorporated into U.S defense thinking. We have heard such comments repeatedly at several of the defense related conferences we recently attended. It is quickly becoming imperative that the U.S. and allied forces have a second set of eyes in every global theatre not subject to the same ground-based risks seen in the Middle East.

Our legacy missile defense systems—often composed of ground radar, GEO (Geosynchronous Equatorial Orbit) satellites, and terrestrial interceptor batteries—are designed to neutralize traditional short- and long-range missiles. The trajectory of these missiles is predictable from shortly after launch, making them relatively straightforward to intercept.

However, newer long-range missiles, such as hypersonic and advanced ICBMs, can change trajectory during travel, and sometimes include decoys and multiple warheads made to fool existing missile defense systems. This makes these missiles much more challenging to neutralize. The U.S. and its allies are vulnerable to these advanced weapons and need a faster, more accurate, and more distributed missile defense system in response.

The unprecedented size and power of AST’s LEO (Low Earth Orbit) satellites make them especially well-suited to assist in tracking modern missiles, along with a variety of other high value functions. Research reveals excellent effective isotropic radiated power (output power of a signal when it is concentrated into a smaller area by the antenna) and gain-to-noise temperature (how well the system can detect weak signals amidst noise), enabling a variety of novel capabilities.

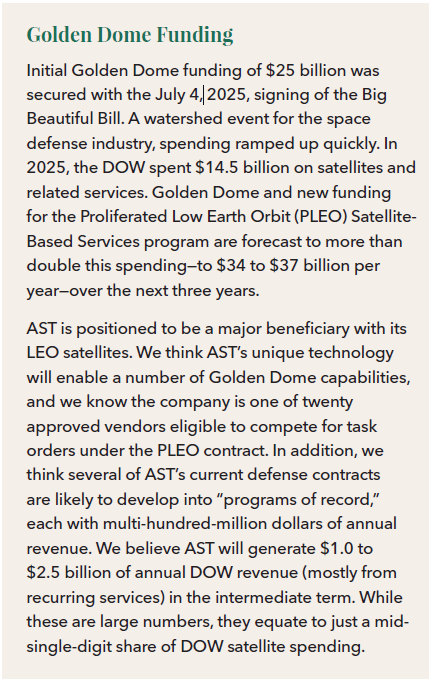

AST’s work with the Federal government continues to build with both defense and communications applications in various stages of testing and development. In terms of defense, AST was awarded a contract with the Missile Defense Agency’s (SHIELD) program, which is part of the broader Golden Dome strategy, focused on building resilient, layered protection against air, missile, space, cyber, and hybrid threats from all operational domains. The selection positions AST SpaceMobile to compete for a wide range of future task orders across research, development, engineering, prototyping, and operations of critical Missile Defense Agency systems that support U.S. national security objectives.

Additional U.S. Department of War (DOW) uses include:

• Radar – Supporting high-value military radar applications such as synthetic aperture radar (high-resolution imaging using radar signal reflections), ground-moving target indication, and missile tracking.

• Assured and Alternative PNT (Position, Navigation, and Timing) – Providing a stronger, jam-resistant signal compared to existing GPS, improving indoor reception and cybersecurity through authentication and encryption.

• Blue Force Tracking (BFT) & Identify Friend or Foe (IFF) – Improving situational awareness of troop and asset locations, reducing friendly fire incidents.

• UAS/Drone Control – Enabling remote control of unmanned aerial systems (UAS) in areas lacking terrestrial infrastructure.

• Signal Intelligence – Detecting and reading electromagnetic emissions of the enemy.

• Signal Jamming – Jamming enemy signals over large geographical areas, such as maritime zones and remote areas, where terrestrial jammers are impractical.

Europa Track 2 Opportunity

In February, AST entered into an agreement with the United States Space Development Agency (SDA) for the Europa Track 2 Commercial Solutions program. The agreement has a total contract value of approximately $30 million. The Europa Track 2 effort is focused on delivering immediate, operationally relevant tactical communications capabilities to U.S. forces around the globe. While just an initial agreement, successful trials could lead to large, recurring government service contracts that harness the dual-use BlueBirds’ global reach, broadband capabilities and encrypted communications.

First Responder Opportunity

AST is also poised to enable supplemental coverage for U.S. first responders (law enforcement, fire/rescue, EMS, emergency management) who require full geographic coverage and 100% uptime, including during natural disasters, in order to provide mission-critical services.

AST is partnered with both AT&T and Verizon, and integration continues with AT&T’s FirstNet partnership in the U.S. AST recently announced a Definitive Agreement with Singapore’s DSTA (Defence Science and Technology Agency) which builds on a previous MOU and we believe AST is working with numerous MNOs and or governments in Europe, the Middle East and Central and South America to expand public safety connectivity. We believe these hybrid-partnerships will be an important and stable part of their business going forward.

International Opportunity

Most developed nations will want defense and emergency services capabilities similar to the U.S. For example, we understand that NATO’s future SATCOM program is actively exploring using AST for 5G direct-to-device service. And Vodafone, AST’s joint venture partner in Europe, offers mission critical emergency services to first responders. They plan to add direct-to-device mobile broadband satellite services to this offering across the EU when it is available through their Satellite Connect Europe joint venture.

To estimate AST’s non-U.S. defense opportunity, we begin with our U.S. DOW revenue estimate of $1.0 to $2.5 billion per annum. We haircut this by half to reflect smaller NATO and non-NATO allied nation defense budgets (cumulatively $0.5 trillion vs. $1.0 trillion at DOW), and adjust further because these nations will likely spend a lower percentage of their budgets on satellite capabilities, leveraging the U.S. Golden Dome where permitted. In total, we estimate that AST will generate $300 to $750 million in annual revenue from non-U.S. defense spending in the intermediate term.

To estimate AST’s non-U.S. first responder opportunity, we begin with our U.S. first responder revenue estimate of $720 million per annum. We adjust our U.S. number to account for differences in population and GDP (across all developed nations, ex-China) and further adjust for the likelihood that AST will have lower first responder market share internationally. In total, we estimate that AST will generate $400 million in annual revenue from non-U.S. first responders in the intermediate term.

Total Military, Intelligence, and First Responder Opportunity

In total, as previously itemized, we expect AST will generate $2.4 to $4.4 billion in annual revenue from worldwide military and first responder opportunities in the intermediate term.

Beyond this, the U.S. National Intelligence Program has a budget of about $80 billion (vs. about $1 trillion at the DOW), which we do not specifically account for in this exercise. That said, it seems clear that many of the capabilities that AST is potentially providing to the DOW would also be valuable to intelligence agencies both here and abroad.

Strides Made in AST’s Satellite Fleet

Over the course of 2025, AST made enormous strides in the design, construction and assembly of its full-size (2,400 SF) dual-use, low-band communication satellites that will become the backbone of its fleet. In December 2025, after the successful launch of the first, full-sized Block 2 Bluebird 6 satellite, AST announced that it had stabilized the spacecraft and fully deployed its massive phased array. Our discussions with the company lead us to believe the satellite is performing as expected mechanically. The next step is to dial-in the software used to control beamforming and RF transmissions. This requires an iterative process that involves software elements that control the satellite, the ground station antennas and AST’s equipment that interconnects with the MNO’s core network. Though time consuming, these learnings will be adapted across all the satellites launched in the coming years.

A Short-Term Setback

In February 2026, AST shipped B2BB 7 to Cape Canaveral for launch on a Blue Origin New Glenn rocket in mid-April 2026. A successful launch on a New Glenn rocket would represent the third global launch provider AST can use for launch services and an important milestone as AST seeks to diversify its service provider network and keep multiple parties competing for its launch business. Though the boost stage worked flawlessly, the second stage failed to lift B2BB 7 to its intended orbit. While the satellite separated from the launch vehicle and powered on, the altitude was too low to sustain operations. Consequently, the satellite was de-orbited a few days later and burned up in the atmosphere. One consolation is that the cost of the satellite is expected to be recovered under an insurance policy. The FAA is leading an investigation into the second stage failure and it may be a month or more before the findings are released and Blue Origin’s modifications are approved and implemented. Blue Origin is slated to be an important provider of launch services in the second half of the year for AST but a thorough investigation is warranted before they can resume launches from Florida.

AST is currently in production through BlueBird 32 with BlueBirds 8 to10 expected to be ready to ship to Cape Canaveral by mid-May with production and launch cadence picking up from there. As they ramp to six satellites per month, AST should be able to build and launch approximately 45 satellites this year which would result in activation of nearly continuous service in the U.S., as well as parts of Europe, Japan and the Middle East. Their goal remains a constellation of approximately 90-95 B2BBs in service by year end 2027.

In the spectrum arena, the company continues its global efforts. They reached a successful conclusion of the Ligado litigation which will allow AST access to North American L-band MSS for its Block 3 BlueBird satellites, the first of which is expected launch at the end of 2026 or early 2027. The B3BBs will use mid-band spectrum (both L & S- band) that will allow more data throughput at faster speeds than the B2BBs. Block 2s are more coverage focused while Block 3s are more capacity oriented. AST is pursing 2GHz S-band spectrum in Europe through regulatory channels and its partnership with Vodafone and is working on MSS applications in Brazil, Mexico and other international locations.

Update on Competition

Starlink, a satellite internet constellation wholly owned by aerospace company SpaceX, is best known for its satellite to home internet service. But four years ago, Starlink teamed with T-Mobile USA to develop and launch a new and well-funded direct-to-cell competitor to AST. However, Starlink’s planned direct-to-cell voice and data service is now limited to simple text messaging, location sharing, and a few essential apps that offer VOIP but no broadband or internet connectivity. To work, the service requires users be outdoors with a direct view of the sky while their handoff puts a heavy strain on a cell phone’s battery. Starlink plans a reboot with newly designed direct-to-cell satellites with new capabilities. These are expected to launch on its larger Starship rocket after receiving regulatory approval.

In April, Amazon announced that it will acquire Globalstar, a mobile satellite services operator known for powering Apple’s Emergency SOS feature, in a $12bb transaction expected to close in 2027. This text only direct-to-cell offering will be paired with Amazon LEO, Amazon’s satellite to home internet service whose satellites are just now being launched. Amazon LEO will ultimately consist of thousands of satellites and compete directly with Starlink’s satellite to home internet services. It will likely be 2-5 yrs before Amazon LEO has the capacity or coverage to compete with Starlink on home internet services. And we believe that AST will not see any additional competition from a revamped or reconstituted Amazon / Globalstar based direct-to-cell service before 2030.

We believe Amazon will receive the necessary regulatory approvals over the next year to acquire Globalstar based on recent comments by Federal Communications Commission (FCC) Chairman Brendan Carr who went on record saying he supports three direct-to-cell competitors in the U.S. The question remains, will Amazon/Globalstar remain a bolt on service with the MNOs (like Starlink direct-to-cell or Apple SOS today) or will it take the much more difficult route over the remainder of the decade of engineering a service that integrates into an MNO’s core network as AST has already done.

Excellent Management

Supporting our view, we believe that AST founder, Chairman, and CEO, Abel Avellan, has assembled a first-class space and wireless technical team, paired with strong commercial, regulatory and legal talent. They have now put in place a team of close to 2,000 employees in five countries. Over the last five years, we have had the opportunity to meet many of their senior leaders, engineers, scientists and Midland factory employees during our visits to headquarters in Midland, Texas and during the launch events in Cape Canaveral. In addition to their employee growth, AST continues to add industry thought leaders and partners to its Board of Directors.

Summary

The last six months showed increasing operational momentum, growing government interest, artful balance sheet management and new company forecasts of revenues approaching $1 billion in 2027, the first full year of continuous coverage across key markets. The company recently filed to increase its constellation shells to four and its satellite count from 248 to 543 at the ITU (International Telecommunications Union). These planned satellites will now include Mobile User Objective System (MUOS) augmentation bands, low-band and S-band capabilities and circle the globe in staggered attitudes up to 740km in two new inclinations of 40- and 55-degrees - including up to 28 sun synchronous and 18 equatorial satellites. Look for more information flow from Europe around their work with Vodafone on IRIS2, Satellite Connect Europe and S-band allocations over the course of the year. In the U.S., the FCC has granted AST full commercial authorization to deploy its initial shell of 248 non-geostationary satellites while the ITU application to expand to 543 is pending.

We continue to believe we are on the cusp of a new communication revolution with decades of potential growth in front of it, and believe AST will play an integral role. AST is a “special situation” investment for the Hennessy Focus Fund, as it does not meet the Fund’s typical compounder model of historically producing a sustained mid-teens or higher rate of earnings growth. However, we believe it presents a very compelling “emerging compounder” profile with a favorable risk-return profile at today’s price.

- In this article:

- Domestic Equity

- Focus Fund

You might also like

-

Fund Commentary

Fund Commentary

Cornerstone Growth FundA Fund Focused on Valuation, Growth and Momentum

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the Hennessy Cornerstone Growth Fund discuss the Fund’s formula-based investment strategy and how it drives the Fund’s sector and industry positioning.

-

Fund Commentary

Fund Commentary

Focus FundHigh Conviction on Companies’ Long-term Future Earnings Power

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers review the second quarter market and the influence of elevated inflation, rate hikes, the development of AI, and what gives them confidence in the portfolio’s ability to continue compounding earnings.

-

Fund Commentary

Fund Commentary

Focus FundRecognizing the Future Earning Power of High-Quality Businesses

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers discuss adding to positions in the first quarter, assess geopolitical impacts on holdings, review AST SpaceMobile developments, and highlight opportunities in a market shaped by factor-driven flows and short-term narratives.