Portfolio Drivers: Consumer Discretionary and Industrials

Cornerstone Mid Cap 30 Fund Portfolio Managers Ryan Kelley and Josh Wein review the Fund’s investment strategy, discuss the most recent rebalance, and highlight the recent change in market cap range of potential investments.

-

Neil J. HennessyChief Market Strategist and Portfolio Manager

Neil J. HennessyChief Market Strategist and Portfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

Key Takeaways

» The strategy seeks 30 mid-cap stocks between $2 and $25 billion in market capitalization with value and momentum characteristics.*

» The Fund’s market cap range has been increased to enhance the opportunity set for the portfolio.

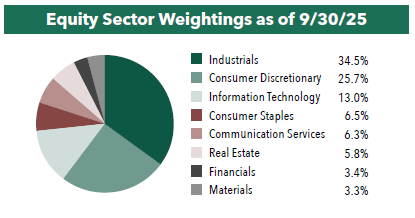

» Following its most recent rebalance, the portfolio is diversified across 8 of 11 sectors; its largest weighting is in Industrials.

» Drivers of performance over this next year could be the overall growth of the economy, the health of the consumer, and continued domestic investment in manufacturing, construction, and energy.

» The Fund’s median price-to-sales ratio is 1.1x as of September 30, 2025, compared to the Russell Midcap® Index’s 1.7x.

* As of September 3, 2025, the market capitalization range changed from $1 to $10 billion to $2 to $25 billion.

What is the Fund’s investment strategy?

The Cornerstone Mid Cap 30 Fund utilizes a formula to select 30 domestic, mid-cap stocks with market capitalizations between $2 and $25 billion that exhibit both value and momentum characteristics. The formula selects stocks with higher year-over-year earnings, positive stock price appreciation, and lower price-to-sales ratios. The universe of mid-cap stocks is screened using these criteria, and the portfolio is rebalanced annually, generally in the fall. Each stock is weighted equally at approximately 3.3% of the portfolio at the onset of the rebalance, although stock price movements can cause relative weights to change over time.

What is the median market capitalization of the Fund’s holdings following the most recent rebalance?

Beginning with this year’s rebalance, the Fund selects its holdings from a universe of stocks with market capitalizations ranging from $2 billion to $25 billion, up from a range of $1 billion to $10 billion. As of September 30, 2025, the median market cap of the Fund was $7.8 billion, up from last year’s $5.5 billion at the end of the rebalance in 2024 and about 75% of the 5-year average market cap of the Russell® Midcap Index. We continue to believe that small to mid-cap stocks offer attractive returns as well as diversification compared to the larger stock universe.

What is the reason for increasing the market cap range of the Fund?

At its inception in 2003, the Mid Cap 30 Formula (the “Formula”) used a market capitalization range of $1 billion to $10 billion. Since that time, the market cap of the overall mid-cap universe has increased substantially. For example, the average market cap of the Russell Midcap® Index was approximately $12.0 billion as of September 30, 2025, up from approximately $2.7 billion in 2003. As a result, with the latest rebalance, we have increased the market cap range of the Formula. We believe the Fund’s revised mid-cap range includes the vast majority of mid-cap stocks in our selection universe.

What potential advantages does the market cap range increase provide investors?

Importantly, we believe this change enhances the opportunity set of attractive companies for inclusion in the Fund. This change also provides other potential advantages as follows:

• Increased Flexibility to Invest in Smaller Market Cap Companies: Increasing the minimum market cap to $2 billion will allow the fund to more easily own smaller market cap companies. When purchasing a new position or adding to an existing position in the Fund, our goal is to purchase no more than 4.9% of any security. Increasing the bottom end of the range from $1 billion to $2 billion means the Fund could invest significantly more into the smallest market cap companies as assets of the Fund grow.

• Lower Liquidity Risk: With a higher minimum market cap as well as a much higher maximum, the liquidity profile of the Fund should improve. An increase in the minimum market cap should help to minimize trading friction inherent in the small-cap market.

Would you please discuss the composition of the Fund?

Following the most recent annual rebalance in the fall of 2025, the Fund’s holdings include stocks representing eight of the 11 GICS (Global Industry Classification System) sectors except Energy, Health Care, and Utilities. The largest sector exposure is Industrials with 10 holdings, and the second largest is Consumer Discretionary with eight holdings. This year, we retained four out of the 30 holdings from last year’s portfolio, which we refer to as “keepers,” including The Cheesecake Factory (CAKE), Dycom Industries, Inc. (DY), Granite Construction, Inc. (GVA), and Peloton Interactive, Inc. (PTON). Finally, while the Fund overall remains highly concentrated in merely 30 stocks, we note that this year’s portfolio is diversified across 23 different GICS sub-industries.

Compared to the Russell Midcap® Index, Industrials is the most overweight sector compared to the benchmark. We believe Industrials could continue to benefit from an improving economy, continued domestic investment in manufacturing, construction, and energy, and strong demand for consulting, air services, and ride-sharing services. Consumer Discretionary is the second most significantly overweight sector. If the consumer remains healthy and wage growth can keep pace with inflation, we believe this could continue to drive spending, which in turn may drive higher growth in earnings and positive stock price performance for many of the Fund’s consumer-related holdings, including restaurants, auto dealerships, and auto parts, home furnishing, footwear and broadline retailers.

Are there common investment themes in the current portfolio?

With over half of the portfolio concentrated in the Industrials and Consumer Discretionary sectors, we believe that primary drivers of relative performance this year will include the overall growth of the economy as well as for the health of the consumer. With the Federal Reserve initiating its first of potentially many rate cuts in September 2025, we believe some relief may be felt by the U.S. consumer. Additionally, if inflation remains moderate, this could lead to improved corporate profitability for many companies that have seen costs rise over the past few years.

Would you please discuss the relative valuation of the Fund’s holdings compared with the benchmark?

Attractive valuation is an important part of the Fund’s stock selection process. The Fund uses price-to-sales as its primary valuation metric because it is a simple metric, it can be universally applied, and it is difficult for companies to manipulate. The Fund selects stocks with price-to-sales ratios below 1.5x. The median price-to-sales ratio of the portfolio is 1.1x as of September 30, 2025, compared to 1.7x for its benchmark index, the Russell® Midcap Index.

- In this article:

- Domestic Equity

- Cornerstone Mid Cap 30 Fund

You might also like

-

Fund Commentary

Fund Commentary

Cornerstone Growth FundA Fund Focused on Valuation, Growth and Momentum

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the Hennessy Cornerstone Growth Fund discuss the Fund’s formula-based investment strategy and how it drives the Fund’s sector and industry positioning.

-

Fund Commentary

Fund Commentary

Focus FundHigh Conviction on Companies’ Long-term Future Earnings Power

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager Brian Macauley, CFACo-Portfolio ManagerRead the Commentary

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers review the second quarter market and the influence of elevated inflation, rate hikes, the development of AI, and what gives them confidence in the portfolio’s ability to continue compounding earnings.

-

Company Spotlight

Company Spotlight

Focus FundAST SpaceMobile: Transforming How the World Connects

David Rainey, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio ManagerRead the SpotlightAST is building the first and only space-based cellular broadband network accessible directly by everyday smartphones with both commercial and government applications. With strategic investments from leading technology players such as AT&T, Verizon, Vodafone and Google, AST has the bold goal to provide uninterrupted broadband connectivity, everywhere.