Banking on Continued Growth

Despite exceptional YTD performance, Financials sector stocks are trading at a historically low relative discount to the market. The banking industry is healthy, and a number of catalysts, including robust M&A activity, higher interest rates, and accelerated loan growth, could push bank stocks higher.

-

David EllisonPortfolio Manager

David EllisonPortfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

We believe banks are poised to profit amid favorable industry tailwinds and a robust economic recovery.

Key Takeaways

» The U.S. economy is setting a solid foundation for bank lending and loan performance

» Banks are positioned to post better net interest income and net interest margins (NIM) going forward

» A robust deal environment could reshape the banking ecosystem as banks acquire new technology and consolidate competitors on a regional and national basis

» It’s all relative—banks continue to trade at a material discount to the market

Favorable Economic Backdrop

A sustained U.S. economic recovery and positive outlook for GDP growth continue to support a healthy operating environment for banks. As overall confidence improves, the supply of credit and the demand for credit should grow accordingly, while the volume of non-performing loans decreases.

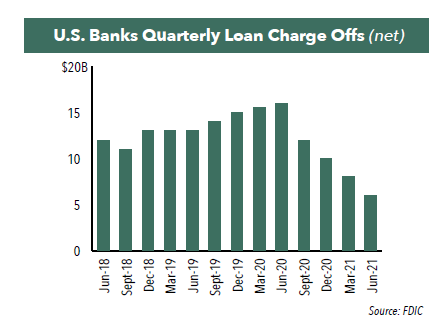

Since the peak of the pandemic in the summer of 2020, overall loan performance has continuously improved. As noted in The Wall Street Journal on October 14, 2021, “Bank profits soared in the latest [third] quarter in large part because the U.S. economy bounced back so quickly from the pandemic recession. Banks last year set aside billions of dollars to prepare for a wave of loan defaults, but now they are releasing the money they had socked away.” Because of the lower-than-expected non-performing loans, we expect net charge-offs will remain at low levels potentially for years to come.

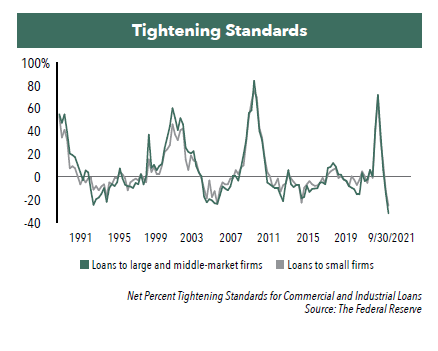

Additionally, there is more evidence that banks are gaining confidence in the recovery and seeking to stoke demand for new loans. The Federal Reserve’s latest loan officer survey demonstrates that bankers are increasingly loosening their lending standards with more favorable terms and better pricing for consumer and commercial loans. A favorable lending environment should be supportive of overall loan growth going forward.

Top-Line Growth Is Poised to Persist Alongside Improved Margins

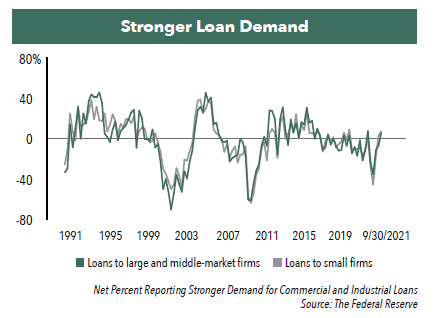

Banks’ net interest income growth is generally propelled by growth in loans outstanding and higher net interest margins. While loan growth has been tepid, growth is showing signs of re-emerging as demand increases across commercial and consumer categories.

Robust loan growth could help bolster the earnings at large national banks that have already benefited from tailwinds in their asset management and capital markets businesses. Furthermore, should interest rates continue to rise alongside a steeper yield curve, bank shares should be rewarded.

Banks Have Improved Their Operating Leverage

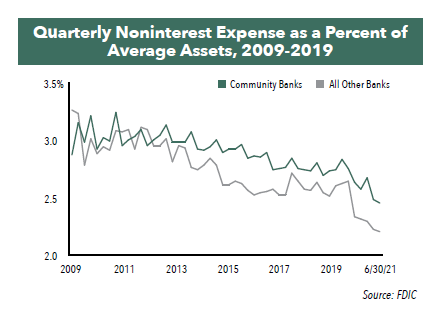

Banks continue to improve their operating leverage with efficiencies in digital and mobile banking buildouts as well as through capital return to shareholders. Since the global financial crisis, banks have consistently reduced their expense base.

Further capital investments in digital banking self-service should drive long-term value for banks. Given branches were accessible in a limited capacity during the pandemic, this led to an acceleration of digital use. Further, digitization and automation of banking will decrease high-cost/low-value transactions, satisfy the generational preferences of new customers and ultimately reduce the costly physical footprint of many banks. Branch counts across the country continue to trend lower, falling from a high of more than 85,500 in 2009 to less than 75,000 as of year-end 2020.

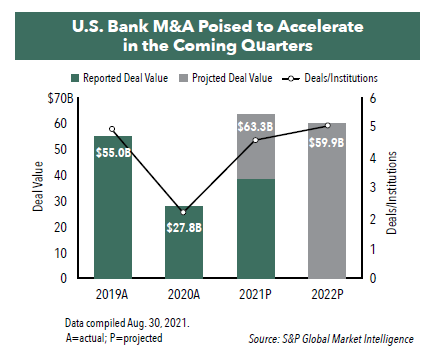

M&A Momentum Is Poised to Continue

Cash-rich banks will likely continue to be acquisitive, as the drive for scale continues and banks seek to deepen their digital banking, wealth, and asset management capabilities. In August 2021, 19 bank transactions were announced, amounting to an aggregate deal value of more than $12 billion. Year-to-date, 2021’s total transaction value has already reached $52 billion, nearly double 2020’s full-year total. Prior to 2019, the last time U.S. bank M&A transactions topped $50 billion was in 2007.1

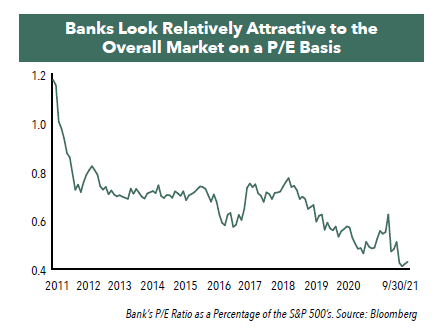

Attractive Relative Value Opportunity

As of October 21, 2021, the S&P 500® Index is trading at 25 times earnings, while the KBW Bank Index is trading at nearly 11 times. Though banks traditionally trade at a discount to the market, current levels are well below historical norms, suggesting both regionals and money center banks have room to grow into a higher multiple.

Benefits of Active Management Within the Financials Sector

With bottom-up research, we seek to own a select group of companies that we believe offer the best opportunity within the Hennessy Large Cap Financial Fund and Hennessy Small Cap Financial Fund’s universe of 400-500 investable companies. The Funds maintain highly concentrated, high conviction portfolios, which may provide the opportunity to outperform the overall sector.

- In this article:

- Financials

- Small Cap Financial Fund

- Large Cap Financial Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Large Cap Financial FundSmall Cap Financial FundSolid Industry Fundamentals & Continued Consolidation

David EllisonPortfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio ManagerRead the CommentaryPortfolio Managers Dave Ellison and Ryan Kelley review 2025 bank performance, fintech-driven consolidation, attractive valuations, and their constructive 2026 outlook.

-

Portfolio Perspective

Portfolio Perspective

Large Cap Financial FundSmall Cap Financial FundSeeking Innovation in the Financials Industry

David EllisonPortfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio ManagerRead the CommentaryPortfolio Managers Dave Ellison and Ryan Kelley discuss what’s driving performance in the Hennessy Large Cap Financial Fund, how tariff increases affect banks, the interest rate environment, and the opportunities in financials.

-

Viewpoint

ViewpointNavigating the Financial Landscape in 2025

David EllisonPortfolio ManagerWatch the VideoHennessy Funds Portfolio Manager Dave Ellison discusses the key drivers behind the financial sector's strong performance in 2024, the impact of potential rate cuts and regulatory changes, and the evolving landscape of banking in 2025. He also explores the challenges and opportunities facing both large and small banks, the role of AI, and the critical risks to watch, from traditional credit concerns to transformative technological shifts.