Favorable Catalysts Driving Energy Companies

Portfolio Manager Ben Cook, CFA discusses his thoughts on the Energy sector in 2021, the effect of a Biden administration on the industry, renewable energy, and midstream companies’ valuations.

-

Ben Cook, CFAPortfolio Manager

Ben Cook, CFAPortfolio Manager

How do you anticipate the Energy sector to fare over 2021?

We see a number of positive supply and demand factors helping to support the price of crude oil and the broader energy industry through 2021. First and foremost, we believe the distribution of COVID-19 vaccines should help restore a sense of normalcy amongst consumers which in turn should drive a significant economic recovery, implying meaningful growth in energy demand.

On the supply side, the recent surprise cut by Saudi Arabia to limit global crude oil production by one million barrels per day and the pivot of many U.S. energy companies to focus on capital discipline have kept global supplies in check.

On the demand side, the “light blue sweep” of recent elections will likely result in additional government stimulus, in the form of additional direct payments and an infrastructure spending package. This injection of additional capital could strengthen GDP growth over the following few quarters, supporting the appetite for energy in the U.S.

With continued OPEC+ coordination we see global crude oil inventories normalizing to historical average levels late this year, which should preserve the current market balance we’ve seen thus far in 2021. While we anticipate oil prices to range between $50 and $55 over the next few quarters, rapid improvement in macroeconomic conditions could trigger prices to rise further, potentially reaching into the $70 to $75 per barrel range.

What might a Biden administration mean for the energy industry?

With the party change in administration, we foresee policy support for cleaner forms of energy and by contrast, growth impediments to the hydrocarbon energy sector. The prospect of additional economic stimulus also looks likely, which should provide a boost to energy consumption in general.

One of Biden’s first actions as president was to sign an executive order instituting a 60-day moratorium on the issuance of oil and gas drilling leases on federal lands. Biden also revoked the construction permit of the Keystone XL Pipeline, a large crude oil pipeline project intended to link supplies in Canada with the U.S. gulf coast. While meaningful, these actions were widely anticipated by many of the companies we follow, and as a result, measures were taken to avert significant impact on operating activities.

In February, Congress introduced the “Green Act of 2021,” which will extend or expand renewable energy tax credits. This should have a positive impact on energy master limited partnerships (MLPs) that generate renewable-oriented qualifying income from energy property eligible for current Production Tax Credits (PTC) and Investment Tax Credits (ITC).

Also, on a positive note, the administration’s support for significant financial stimulus may spur U.S. GDP growth to between 5% and 6%. This increase in economic growth will require energy of all sorts, including hydrocarbons.

How is the energy industry adapting to the increased demand for renewable energy?

We believe renewable energy sources will play an increasing role in satisfying growing global power demand. However, we recognize many of the renewable sources and technologies are still in the early stages of development and will take time to employ on a scalable basis. As a result, a variety of fuel sources, including oil and natural gas, will continue to make up the global energy mix over the next several decades. Additionally, the primary sources of renewable energy—namely solar and wind power—are intermittent; in other words, the sun doesn’t always shine, and the wind doesn’t always blow. So, there will always be a place for diverse energy sources, and we believe that natural gas, the cleanest of the fossil fuels, will play a key role in the energy transformation.

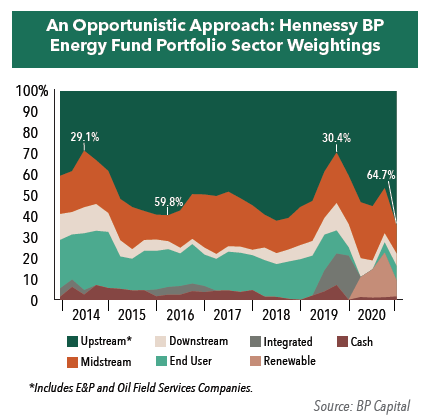

The Hennessy BP Energy Fund seeks to invest in a broad investable universe that is inclusive of both renewable and hydrocarbon-based companies. From time to time, the Fund’s mix of companies will shift as holdings are re-allocated to pursue the most attractive risk-adjusted return opportunity. As indicated in the chart below, the Fund initiated positions in several renewable energy companies that had fallen precipitously amidst pandemic-related market volatility during the first quarter of 2020. More recently, the prospect of rising commodity prices associated with a revived post-pandemic global economy prompted a move back toward traditional hydrocarbon energy.

What do you find attractive about Exploration and Production (E&P) companies?

The portfolio is currently weighted predominantly towards companies engaged in exploring, developing, and producing crude oil and natural gas. In the past, these companies had followed a “spend-for-growth” model, often over-relying on debt issuance to expand production growth. However, in recent years E&P companies have realigned their priorities and moved toward a model of capital discipline. They have adjusted their capital spending plan away from increasing production growth at any price and toward increasing free cash flow and investment returns.

Finally, based on current commodity prices, we see several compelling valuations disconnects given relatively low current E&P company equity values. We believe this gap will ultimately narrow to provide a favorable equity valuation uplift for many of the producers within the portfolio.

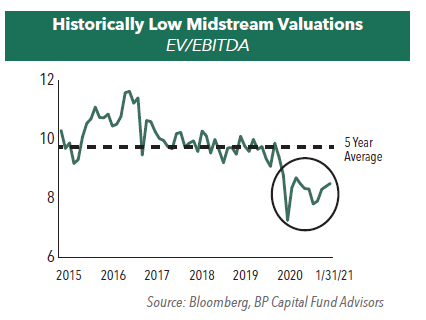

What are the current valuations of midstream energy companies?

We believe midstream companies’ valuations continue to be compelling, trading at discounts to historical valuations even after the recent run-up in stocks. As of 1/31/21, midstream companies traded at approximately 8x their EV/EBITDA, significantly below their pre-COVID-19 multiple of 10x and their 5-year historical average of 11.4x.

Would you please discuss midstream companies’ current cash flow generation?

With a focus on generating internal cash flow and selectivity in their capital expenditures, many midstream companies have entered 2021 with very strong cash flow and balance sheets. In fact, 25 of the 30 largest companies within the midstream sector are expected to generate positive free cash flow in 2021, setting the stage for increased debt reduction and approximately $2 billion in share buybacks across the industry this year. In addition to rewarding investors, these buybacks can be viewed as a strategic decision by midstream companies’ managements to both reduce their outstanding shares and subsequently lower their dividends as a percentage of total cash flow.

- In this article:

- Energy

- Energy Transition Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Midstream FundPotential Natural Gas Tailwinds for Midstream Companies

Ben Cook, CFAPortfolio Manager L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryThe following commentary highlights how recent events in Venezuela affect midstream investors, how midstream companies could benefit from interest rate cuts, rising natural gas and LNG demand, and AI-driven efficiencies, while maintaining disciplined capital allocation, strong shareholder returns, and attractive valuations.

-

Portfolio Perspective

Portfolio Perspective

Energy Transition FundThe Role of Natural Gas to Meet AI Energy Demand

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, Portfolio Manager Ben Cook and Josh Wein highlight the Fund’s 2025 outperformance, discuss the impact the events in Venezuela may have on the energy sector, and outline key 2026 Energy sector opportunities.

-

Portfolio Perspective

Portfolio Perspective

Gas Utility FundNatural Gas Utilities as a Potential Growth Story

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryWith AI-driven power demand, rising capital investments, LNG growth, and pipeline infrastructure expansion, natural gas utilities are being repositioned as potential growth stories with attractive valuations and dividends.