Investing in Higher Profitability Companies at Attractive Valuations

In the following commentary, the Portfolio Managers of the Hennessy Cornerstone Large Growth Fund discuss the Fund’s formula-based investment process and how it drives the Fund’s sector and industry positioning.

-

Neil J. HennessyChief Market Strategist and Portfolio Manager

Neil J. HennessyChief Market Strategist and Portfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

What is the Hennessy Cornerstone Large Growth Fund’s investment strategy?

The Fund utilizes a formula-based approach in building a portfolio of attractively valued, highly profitable, larger-cap companies. In essence, the strategy seeks high quality, high return companies that may be overlooked by investors. From the universe of stocks in the S&P Capital IQ Database, the Fund selects the 50 stocks with the highest one-year return on total capital which also meet the following criteria, in the specified order:

» Above-average market capitalization

» Price-to-cash flow ratio less than the median of the remaining securities

» Positive total capital

Why does the Fund use these screening criteria?

Larger market capitalization companies tend to be well-established leaders in their industries with long, successful track records and solid profitability.

A low price-to-cash flow ratio can be a good indicator of an attractive stock valuation. Positive cash flow tends to be associated with companies with profitable business models.

The use of positive total capital as a screening criterion helps the Fund avoid financially weaker companies.

Why does the formula select stocks with the highest one-year return on total capital?

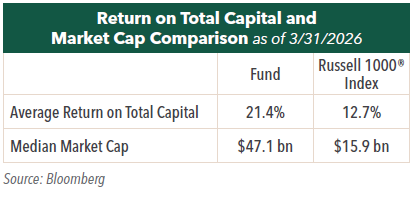

From among the companies that meet the screening criteria, the Fund selects the 50 with the highest one-year return on total capital. We believe return on total capital is an excellent measure of a company’s profitability and is often associated with strong management, high barriers to entry, and other favorable attributes. As a result, we believe this measure can help uncover stocks with the potential to outperform the market.

How does the Fund seek to provide a return to investors?

We believe the Fund’s investments present the potential for capital appreciation when and if market sentiment changes and their valuations rise. Strong profitability has the potential to lead to earnings growth, which could also drive capital appreciation.

How often does the Fund rebalance its portfolio?

The universe of stocks is re-screened and the portfolio is rebalanced annually, generally in the winter. Holdings are weighted equally by dollar amount with approximately 2% of the Fund’s assets invested in each during the rebalance.

How does the Fund’s portfolio differ from its benchmark?

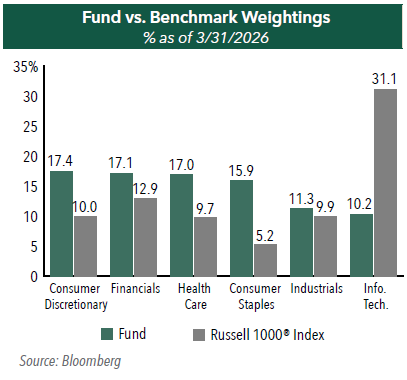

Almost 70% of the Fund is invested across four sectors: Consumer Discretionary, Financials, Consumer Staples, and Health Care. Compared to its benchmark, the Russell 1000® Index, the Fund is most significantly overweight Consumer Staples and Consumer Discretionary and most significantly underweight Information Technology. The Fund is invested in nine of the 11 GICS sectors, apart from Real Estate and Utilities.

What are some significant drivers of the Fund?

Many companies in the portfolio are dependent on the consumer, with 33% concentrated in Consumer Discretionary and Consumer Staples. Our consumer related holdings cover many individual subindustries, including staples such as food retail and distribution, household products, and soft drinks and other beverages. Our Consumer Discretionary holdings include companies in apparel, automotive, broadline and specialty retail, home-related retail and homebuilding, and restaurants. Financials are also a large part of the portfolio, with nine holdings spread across asset management, insurance, and transaction and payment processing.

While there is evidence of increasing stress due to rising costs for the consumer, overall consumer spending remains solid and could continue to be a significant driver of the Fund. Consumer stocks may see positive performance as consumers, buoyed by a stable labor market and rising wages, are likely to increase spending on both essential and nonessential goods and services. Financials tend to be less cyclical and could benefit from strong underwriting and increased volumes of consumer transactions. While policy and global disruptions may affect companies in the portfolio, we continue to see value in investing for the long-term based on fundamentals and not on fluctuating or unpredictable trends.

- In this article:

- Domestic Equity

- Cornerstone Large Growth Fund

You might also like

-

Fund Commentary

Fund Commentary

Cornerstone Growth FundA Fund Focused on Valuation, Growth and Momentum

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the Hennessy Cornerstone Growth Fund discuss the Fund’s formula-based investment strategy and how it drives the Fund’s sector and industry positioning.

-

Fund Commentary

Fund Commentary

Focus FundHigh Conviction on Companies’ Long-term Future Earnings Power

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager Brian Macauley, CFACo-Portfolio ManagerRead the Commentary

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers review the second quarter market and the influence of elevated inflation, rate hikes, the development of AI, and what gives them confidence in the portfolio’s ability to continue compounding earnings.

-

Company Spotlight

Company Spotlight

Focus FundAST SpaceMobile: Transforming How the World Connects

David Rainey, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio ManagerRead the SpotlightAST is building the first and only space-based cellular broadband network accessible directly by everyday smartphones with both commercial and government applications. With strategic investments from leading technology players such as AT&T, Verizon, Vodafone and Google, AST has the bold goal to provide uninterrupted broadband connectivity, everywhere.