Recognizing the Future Earning Power of High-Quality Businesses

The Portfolio Managers discuss adding to positions in the first quarter, assess geopolitical impacts on holdings, review AST SpaceMobile developments, and highlight opportunities in a market shaped by factor-driven flows and short-term narratives.

-

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager -

Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager -

Brian Macauley, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio Manager

Key Takeaways

» As market leadership broadened, high-quality companies were priced as if their long-term value vanished due to broader industry fears.

» We believe the portfolio is well positioned to benefit from potentially lower oil prices and a pickup in economic growth over the medium to long term.

» AST’s work with the Federal government continues to build with both defense and communications applications in various stages of testing and development.

» We believe the most supportive aspect of today’s U.S. equity market is the extraordinary pace of innovation driven by accelerating technological change.

How has expanding market leadership beyond mega-cap tech changed portfolio opportunities?

While much has been made of the recent cooling in mega-cap technology, the true “widening” of the market has less to do with the giants stumbling and more to do with the indiscriminate selling of high-quality businesses caught in the crosshairs of macro narratives. We have long argued that volatility is the friend of the long-term investor, and the recent environment has been a textbook example. As leadership began to broaden, it unearthed a paradox: world-class companies with durable moats were being priced as if their terminal value had vanished overnight, simply because they shared a zip code with broader industry fears.

The software sector, in particular, bore the brunt of an “AI eats software” mentality. A wave of anxiety suggested that AI would immediately commoditize legacy software and erode development barriers, leading to a sharp downdraft across the space. This created a compelling entry point for us in Altus Group. While the market fretted over generalized disruption, we saw a mission-critical service provider with proprietary data and deeply embedded workflows that AI is more likely to enhance than replace. By focusing on the resilience of their business model rather than the prevailing narrative, we were able to add to our position at a significant discount to its long-term intrinsic value.

Similarly, we found rare value in the alternative asset management space, where Brookfield Asset Management was unfairly penalized by a growing “private credit contagion” narrative. Fears that deteriorating credit in software-related private lending would trigger a wider liquidity crisis led to a reflexive sell-off across the sector. In our view, this was a classic case of the market mispricing risk by ignoring the strength of a best-in-class manager with a diversified global footprint and a massive dry powder advantage. By leaning into these artificial intelligence and credit-related fears, we have been able to high-grade the portfolio with durable, compounding businesses at valuations that we believe set the stage for strong future returns.

Over the quarter, which holdings contributed the most to performance and which detracted the most?

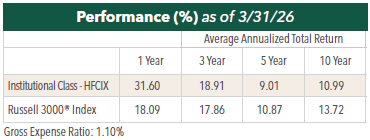

The biggest contributors to Fund performance during the quarter were AST SpaceMobile (+14.1%), Applied Materials (+33.1%), and Shenandoah Telecom (+33.4%). The biggest detractors from Fund performance during the quarter were Brookfield Corporation (-11.7%), Markel Group (-11.0%), and Ashtead Group (-7.5%).

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting hennessyfunds.com.

How are you evaluating geopolitical developments for the companies you own?

The 50%+ increase in oil prices in the first quarter, with both direct as well as tangential inflationary impacts, has taken the expectation of multiple Federal Reserve rate cuts off the table for the year. Gas price increases to Americans are like an across-the-board tax increase and especially impactful on low-, moderate-, and middle-income consumers who are forced to reprioritize spending. This general impact is even higher in Europe and developing markets in Asia given their dearth of domestic oil production, while in the U.S. we remain a net exporter of oil and have not absorbed the same impacts as those overseas. Accompanying this oil shock was an increase in both short and long-term interest rates.

Given this backdrop, over the course of the year we believe the Fund’s consumer-facing businesses (such as CarMax, RH and NVR) will continue to see weakened consumer demand driven by reprioritized spending as well as overall demand destruction from higher financing rates used by many of their customers. Over the intermediate and long-term, we believe the portfolio is well positioned to benefit from declining oil prices later in the year as well as a pickup in economic growth like what the U.S. enjoyed just a few months ago as underlying economic elements and psychology remain in place for sustained Gross National Product (GNP) growth.

What role is AST SpaceMobile playing in U.S. defense strategy given the Middle East conflict?

If the war in Iran has taught us anything it is that ground-based radar is vulnerable to missiles and drones guided by satellite systems. Without ground-based radars our defensive interceptors are blind. This vulnerability is being rapidly incorporated into U.S defense thinking. We have heard such comments repeatedly at several of the defense related conferences we recently attended. It is quickly becoming imperative that the U.S. and allied forces have a second set of eyes in every global theatre not subject to the same ground-based risks we have seen in the Middle East.

In this vein, AST’s work with the Federal government continues to build with both defense and communications applications in various stages of testing and development. In terms of defense, AST was awarded a contract with the Missile Defense Agency’s (SHIELD) program, which is part of the broader Golden Dome strategy, focused on building resilient, layered protection against air, missile, space, cyber, and hybrid threats from all operational domains. The selection positions AST SpaceMobile to compete for a wide range of future task orders across research, development, engineering, prototyping, and operations of critical Missile Defense Agency systems that support U.S. national security objectives.

What in today’s U.S. equity market supports and challenges long-term compounders?

From our vantage point, the most supportive aspect of today’s U.S. equity market is the extraordinary pace of innovation driven by accelerating technological change. Entire industries are being reshaped in compressed timeframes, creating meaningful opportunities for well-managed businesses to extend their competitive advantages and reinvest at high rates of return. At the same time, this rapid evolution raises the bar for investors: it requires greater care and humility in assessing which companies truly possess enduring moats and which may be more vulnerable to disruption or obsolescence than they appear.

We also observe a market increasingly influenced by factor-driven flows and short-term narratives rather than underlying business fundamentals. Price movements are often dictated by exposures—growth, value, momentum, or thematic trends—rather than changes in intrinsic value. This dynamic is increasingly evident in the market’s response to perceived tail risks, particularly around artificial intelligence, where investors frequently “shoot first and ask questions later.” As a result, stocks can experience sharp and sometimes indiscriminate repricing based on speculative interpretations rather than sober analysis.

For long-term investors, these conditions create a compelling opportunity set. The combination of rapid technological change and narrative-driven volatility can lead to temporary dislocations that ignore the future earning power of high-quality businesses. Our task is to carefully distinguish between businesses facing genuine structural impairment and those experiencing short-term, sentiment-driven downdrafts in their share prices. When we get that distinction right, periods of market overreaction can provide attractive entry points, ultimately enhancing long-term compounding even in an increasingly noisy and fast-moving environment.

- In this article:

- Domestic Equity

- Focus Fund

You might also like

-

Fund Commentary

Fund Commentary

Cornerstone Growth FundA Fund Focused on Valuation, Growth and Momentum

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the Hennessy Cornerstone Growth Fund discuss the Fund’s formula-based investment strategy and how it drives the Fund’s sector and industry positioning.

-

Fund Commentary

Fund Commentary

Focus FundHigh Conviction on Companies’ Long-term Future Earnings Power

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers review the second quarter market and the influence of elevated inflation, rate hikes, the development of AI, and what gives them confidence in the portfolio’s ability to continue compounding earnings.

-

Company Spotlight

Company Spotlight

Focus FundAST SpaceMobile: Transforming How the World Connects

David Rainey, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio ManagerRead the SpotlightAST is building the first and only space-based cellular broadband network accessible directly by everyday smartphones with both commercial and government applications. With strategic investments from leading technology players such as AT&T, Verizon, Vodafone and Google, AST has the bold goal to provide uninterrupted broadband connectivity, everywhere.