Unlocking Undervalued Potential in Japanese Small Caps

In the following commentary, the Portfolio Managers discuss recent strong performance, the effects of geopolitical tensions, softer Chinese tourism, currency dynamics, rising interest rates, wage negotiations, valuations, and economic drivers for the Fund’s Japanese small-cap holdings.

-

Takenari Okumura, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio Manager -

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Key Takeaways

» We believe investor interest in Japanese small cap equities has been driven primarily by attractive valuation, Japan’s more inflationary economic environment, and improved capital efficiency.

» While we view the economic impact of rising oil prices as largely temporary and driven by geopolitical factors, recent market volatility has created attractive investment opportunities.

» Even though the number of visitors from China has declined, inbound tourism from other regions has increased, elevating overall levels.

» This year marks the third consecutive year of wage increases exceeding 5% during the annual spring labor negotiations.

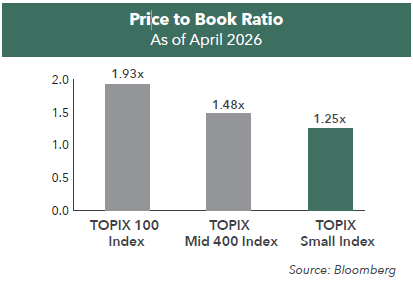

» Japanese small-cap equities trade at an attractive price to book and trade at a discount of more than 30% relative to large-cap peers.

» We see many companies redeploying cash balances into investment initiatives amid rising inflation, with an emphasis on enhancing capital returns.

What factors drove Japanese small caps’ strong performance year-to-date 2026?

The key underlying trends have remained the same as in 2025. Investor interest in Japanese small cap equities has continued to build, driven primarily by:

1. Their relative valuation attractiveness compared with large cap stocks,

2. Japan’s structural shift toward a more inflationary economic environment, and

3. The gradual but broad based improvement in capital efficiency among smaller companies, which had lagged historically.

In addition, amid periods of heightened market volatility triggered by worsening geopolitical tensions in the Middle East, Japanese small caps have experienced relatively less selling pressure, supported by their low absolute valuation levels.

With geopolitical tensions contributing to increased volatility in global markets, what risks and opportunities has this created for the companies in your portfolio?

Japan remains relatively exposed to Middle Eastern geopolitical developments due to its high dependence on crude oil imports from the region. Given the sharp equity market gains earlier this year, we believe Japanese equities have shown heightened sensitivity during recent risk off periods. While the economic impact of rising oil prices is likely to become more visible over time, we view these pressures as largely temporary and driven by geopolitical factors, therefore do not see them as warranting excessive concern at this stage.

In sectors such as construction and banking, where structurally favorable operating environments remain intact, recent market volatility has created attractive investment opportunities. Key risks we continue to monitor include potential deterioration in consumer sentiment stemming from higher energy costs and declines in asset prices.

How have ongoing tensions between Japan and China affected tourism and domestically oriented Japanese companies?

While the number of visitors from China has declined, inbound tourism from other regions—including Taiwan and South Korea—has increased, allowing overall inbound visitor levels to remain elevated. Japan continues to maintain strong appeal as a travel destination. Tourism activity is increasingly extending beyond major metropolitan areas into regional destinations, and we believe inbound consumption will continue to provide underlying support for domestic demand.

However, given the relatively higher per capita spending by Chinese tourists, the impact on luxury consumption—particularly at department stores—is not insignificant. We therefore maintain a cautious stance toward related sectors, and notably, the Fund has already fully exited its holdings in department store stocks.

With respect to domestic consumption, we believe steady wage growth will continue to support a gradual recovery through rising disposable incomes. That said, we remain attentive to the risk that higher oil prices and recent declines in asset prices could weaken consumer sentiment in the near term.

How are currency dynamics affecting the domestic companies the Fund invests in?

Across many of the companies held in the portfolio, we observed that management teams have shown a strong commitment to passing through higher costs—including those associated with yen depreciation—through pricing, in order to protect margins.

We also see the potential for weaker small and medium sized enterprises to exit the market, and as such, do not view continued yen depreciation as a net negative from a medium term perspective.

With the Bank of Japan gradually raising rates, what second-order effects are you watching most closely for Japanese companies and equity markets?

We expect an increase in corporate bankruptcies, particularly among highly leveraged companies with weaker balance sheets. At the same time, we believe that the exit of structurally low profit firms will accelerate a process of competitive rationalization, allowing stronger companies to gain share—representing a positive structural development for the Japanese economy over the medium term.

Would you please discuss the outcome of Japan’s wage negotiations in 2026? How might sustained wage growth influence consumer spending and the outlook for domestically oriented Japanese companies?

This year marks the third consecutive year of wage increases exceeding 5% during the annual spring labor negotiations, reflecting meaningful progress in Japan’s wage growth cycle. Although real wages had remained negative due to inflationary pressures, they turned positive for the first time in 13 months in February. However, rising oil prices have renewed concerns around inflation, which could negatively affect consumer sentiment.

We expect Japanese consumers to continue exhibiting increasingly selective consumption behavior, accelerating divergence between stronger and weaker companies. Within the Fund, we maintain a disciplined approach focused on companies that can effectively communicate and deliver value to customers through product strength, service quality, and brand differentiation.

How are smaller domestic businesses adapting their use of AI, automation, pricing power, or operational changes to maintain profitability?

In labor intensive sectors such as construction, companies are responding through more selective project acceptance and contract redesigns that incorporate cost increases into pricing. These practices are becoming increasingly well established across the industry, contributing to improved profitability.

More broadly, heightened awareness around capital efficiency has led to greater restructuring efforts, including the downsizing or exit of low margin businesses. We view these developments as constructive for corporate earnings sustainability.

Following the continued strong performance of Japanese equities, how do you assess the valuation opportunity in domestically oriented small-cap companies today?

While near term earnings levels remain sensitive to fluctuations in currency and oil prices, there remains significant scope for valuation re-rating driven by ongoing improvements in capital efficiency.

As shown in the below chart, Japanese small-cap equities as measured by TOPIX Small Index of small-caps traded at 1.25x price to book, which we view as attractive in absolute terms. In addition, they continue to trade at a discount of more than 30% relative to large-cap peers, suggesting further room for normalization.

Looking ahead, which domestic economic drivers do you believe will be most important for the Fund’s holdings?

We maintain a cautious stance toward domestic consumption, including inbound demand, given elevated geopolitical risks and the potential for sentiment deterioration resulting from higher energy prices.

On the corporate side, we see a clear and ongoing shift toward redeploying cash balances into investment initiatives amid rising inflation, with an emphasis on enhancing capital returns. This trend is expected to continue.

In addition, company specific actions—such as pricing discipline and more selective order intake—are directly contributing to margin expansion, and we believe these internal initiatives will remain an important driver of earnings growth for the Fund’s holdings.

- In this article:

- Japan

- Japan Small Cap Fund

You might also like

-

Investment Idea

Investment IdeaCompelling Valuations in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Masakazu Takeda, CFA, CMAPortfolio Manager Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment Idea

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaJapanese equities are currently trading at compelling valuation levels compared to other developed equity markets around the world and relative to their own historical averages. We believe the Japanese market deserves a closer look.

-

Investment Idea

Investment IdeaWhy Active Matters When Investing in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaWhen investing in Japanese businesses, we believe it is imperative to select a manager who is immersed in the culture and can perform in-depth, company-specific research to build a concentrated portfolio of Japanese companies that can outperform a benchmark and weather volatility.

-

Company Spotlight

Company Spotlight

Japan FundBerkshire Hathaway’s Stake in Tokio Marine Highlights the Appeal of Japanese Insurers

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio ManagerRead the SpotlightTokio Marine is Japan’s largest general insurance group with a solid track record in the domestic market and an expanding overseas business. Tokio Marine is one of three Japanese insurers that has significant market share and enjoys high profitability and strong pricing power due to industry consolidation—qualities Berkshire Hathaway appears to have noticed.