Berkshire Hathaway’s Stake in Tokio Marine Highlights the Appeal of Japanese Insurers

Tokio Marine is Japan’s largest general insurance group with a solid track record in the domestic market and an expanding overseas business. Tokio Marine is one of three Japanese insurers that has significant market share and enjoys high profitability and strong pricing power due to industry consolidation—qualities Berkshire Hathaway appears to have noticed.

-

Masakazu Takeda, CFA, CMAPortfolio Manager

Masakazu Takeda, CFA, CMAPortfolio Manager -

Angus Lee, CFAPortfolio Manager

Angus Lee, CFAPortfolio Manager

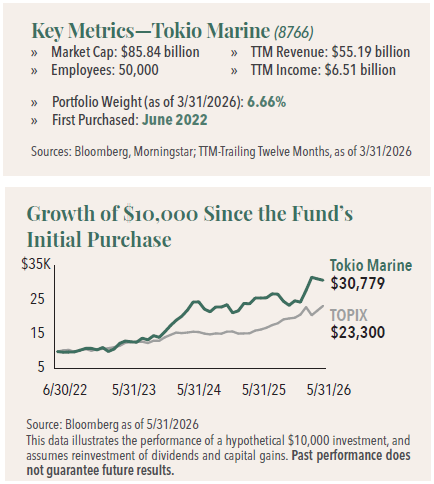

Berkshire’s 2.5% Stake in Tokio Marine

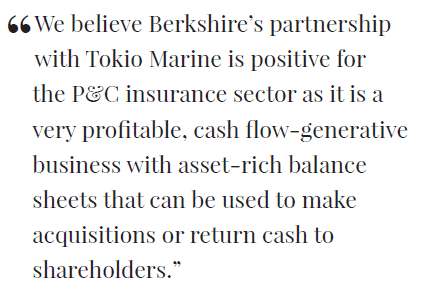

In 2026, Warren Buffett’s Berkshire Hathaway acquired a 2.5% stake in Tokio Marine for approximately $1.8 billion and there are signs of potentially further accumulation. The partnership gives Tokio Marine access to Berkshire Hathaway’s vast capital base, enhancing its ability to pursue larger acquisitions and underwrite opportunities that might otherwise exceed its standalone risk appetite.

Berkshire has consistently partnered with businesses that demonstrate underwriting discipline, conservative risk management, and rational capital allocation, and Tokio Marine meets these criteria.

More broadly, this partnership reinforces the outlook for Japanese non-life insurers. After years of consolidation, the industry has developed stronger pricing discipline, improved balance sheets, and a clearer focus on capital efficiency and shareholder returns. Within this context, Tokio Marine stands out due to its global business mix and consistent execution.

Tokio Marine: One of the World’s Largest and Oldest Insurance Groups

Founded in 1879, Tokio Marine was Japan’s first non-life insurance company and has grown to become one of the largest and longest-standing insurance groups in the world. The company is a collection of insurance businesses and includes over 365 subsidiaries and 33 affiliates in more than 480 cities in more than 50 countries and regions around the world.1

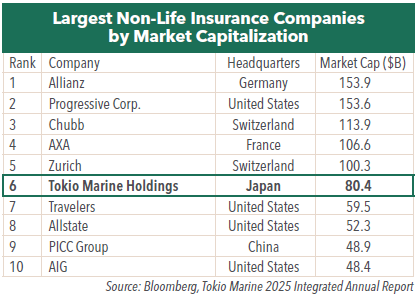

In terms of market capitalization, Tokio Marine was ranked the sixth largest non-life insurance company in the world as of June 2025. Tokio Marine’s CEO Masahiro Koike has set a more ambitious goal: transforming the company into a top-five global insurance group within the next decade.

Expansion of Its International Operations

As an insurance business that underwrites global risks, diversification is the cornerstone of Tokio Marine’s strategy. In fact, Tokio Marine was an international company from its earliest beginnings.

Since the late 2000s, the company has executed a series of acquisitions in specialty insurance markets, including Philadelphia Insurance, Delphi Financial Group, HCC Insurance, and Pure Group.

These transactions have diversified Tokio Marine’s business. Japan is an archipelago prone to earthquakes and typhoons and is also a country with a high ownership of automobiles. As such, the bulk of Japanese insurance portfolios is comprised of auto and fire insurance policies.

As insurance is a business of risk management, Tokio Marine has focused on purchasing overseas insurance businesses where there is a low correlation with natural disasters in Japan. This overseas exposure in the specialty insurance category provides business diversification, which should translate into lower equity risk premium moving forward.

These companies have strong growth potential and high profitability. They also have few overlapping risks with existing businesses and are thus contributing to enhancing capital efficiency, increasing profits, and stabilizing the business platform.

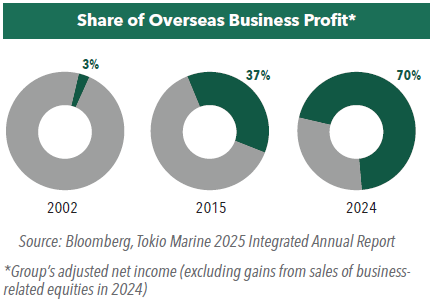

As a result of these acquisitions, 70% of Tokio Marine’s profits originate from overseas operations.

Having successfully transformed itself into a global specialty insurer, Tokio Marine is now focused on expanding its international footprint further and broadening its presence beyond the U.S., which currently accounts for the majority of its overseas earnings.

Shareholder-Friendly Business Practices

Management has continued to make progress on capital allocation. Tokio Marine‘s policy is to sustainably increase dividends per share in line with its profit growth. Following the fiscal year 2025 results announced in May 2026, the company reported a return-on-equity of 19.3% (Consolidated ROE), with management indicating that underlying ROE remains around the low-teens level. Over the same period, the dividend payout ratio was approximately 42%, reflecting continued growth in shareholder distributions supported by earnings and balance-sheet strength.

More importantly, Tokio Marine continues to demonstrate financial flexibility in how it deploys capital. Dividends and buybacks remain key tools when excess capital builds, particularly given the company’s ability to monetize policy shareholdings over time.

The strategic partnership with Berkshire Hathaway should be an important additional lever. By conducting future M&A transactions jointly, Tokio Marine can reduce its standalone capital burden, which should help free up capacity for further dividend growth and share buybacks while also providing a pathway to improve underlying returns on equity over the medium term.

Policy Shareholdings — Unique to Japan

In the 1960s, the non-life insurance companies including Tokio Marine purchased minority shares in other companies to build and maintain business relationships in corporate insurance. These strategic equity holdings, or “policy shareholdings” have large unrealized gains worth billions of dollars today and have been tapped to fund growth. Strong cash flows from market oligopoly, ample proceeds from the periodic sales of equity holdings together with able management teams are factors that give the Japanese insurance companies a competitive edge and makes them uniquely attractive in the global insurance space.

Attractive Valuation and Dividend Yield

Insurance businesses have historically been generally regarded as mundane and mature in Japan. However, since the industry has been growing faster than the country’s GDP, we view Tokio Marine as anything other than mundane.

As of April 2026, Tokio Marine was trading at a price-to-earnings ratio of approximately 13x and a price-to-book ratio of 2.3x–2.5x, while the broader Tokyo Stock Price Index traded at a higher earnings multiple and a lower price-to-book ratio.

In our view, valuation for insurers should be considered primarily in the context of earnings quality, balance-sheet discipline, and capital allocation, rather than viewed in isolation or solely through headline return metrics. Given Tokio Marine’s underwriting discipline and diversified global earnings base, a premium to book value relative to the broader market is reasonable.

At the same time, the company’s earnings multiple remains moderate when viewed alongside the stability and durability of its earnings profile. Therefore Tokio Marine’s valuation appears broadly consistent with its business characteristics, while leaving scope for further improvement if underlying returns strengthen over time.

- In this article:

- Japan

- Japan Fund

1 Source: Tokio Marine Group Overview

You might also like

-

Fund Commentary

Fund Commentary

Japan Small Cap FundSelective Opportunities in Japan’s Small-Cap Market

Takenari Okumura, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio Manager Tadahiro Fujimura, CFA, CMAPortfolio ManagerRead the Commentary

Tadahiro Fujimura, CFA, CMAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers discuss the opportunities emerging in Japan’s small-cap market, highlighting improving corporate profitability, evolving management practices, and attractive valuations in a more selective market environment.

-

Fund Commentary

Fund Commentary

Japan FundIdentifying Select Opportunities in Japanese Businesses

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers discuss Japan’s improving corporate fundamentals, the continued benefits of governance reform, and why stock selection remains essential as the market becomes increasingly differentiated.

-

Investment Idea

Investment IdeaCompelling Valuations in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaJapanese equities are currently trading at compelling valuation levels compared to other developed equity markets around the world and relative to their own historical averages. We believe the Japanese market deserves a closer look.