Portfolio Update April 2019

Cornerstone Value Fund - The Fund's Portfolio Managers discuss the Fund’s quantitative investment strategy, and how it drives the Fund’s sector and industry positioning.

-

Neil J. HennessyChief Market Strategist and Portfolio Manager

Neil J. HennessyChief Market Strategist and Portfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

What is the Hennessy Cornerstone Value Fund’s investment strategy?

The Fund utilizes a quantitative approach to build a portfolio of potentially undervalued, profitable, large-cap companies. From the universe of stocks in the S&P Capital IQ Database (excluding Utilities), the Fund selects 50 stocks with the highest dividend yield which also meet the following criteria:

- Market capitalization that exceeds the average of the Database

- 12-month sales that are 50% greater than the average of the Database

- Cash flows that exceed the average of the Database

- Number of shares outstanding that exceeds the average of the Database

Why does the Fund use these screening criteria?

Each of the first three criteria seeks to help the Fund find companies that are large, profitable and able to pay a healthy dividend.

- Large market capitalizations tend to be associated with companies that are well-established leaders in their industries, with long successful track records and solid profitability.

- A large revenue base tends to be associated with companies that have high market shares or that have diversified successfully.

- Above average cash flow identifies companies with strongly profitable business models, possibly generating excess cash flow, which may be returned to shareholders in the form of a dividend.

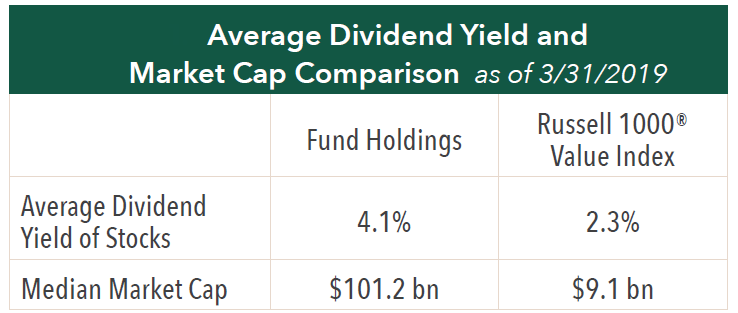

How does the Fund use dividend yield to identify potentially undervalued stocks?

From among the companies that have passed the screening criteria, the Fund then selects the 50 with the highest dividend yield. High dividend yield can be a good indicator of a low stock valuation, therefore, this ranking criterion is designed to uncover potentially undervalued companies.

Why does the Fund rank by and select stocks with an average dividend yield?

From among the companies that have passed the screening criteria, the Fund then selects the 50 with the highest average dividend yield. As high average dividend yield can be a good indicator of a low stock valuation, this ranking criteria helps uncover potentially undervalued companies.

How does the Fund seek to provide a return to investors?

We believe the combination of profitability and value offers investors an opportunity to earn a return in two ways. In our view, the Fund’s investments offer the potential for capital appreciation if and when market sentiment changes and their valuations rise. Investors in the Fund are also “paid to wait,” potentially rewarded with a steady income stream from the dividends.

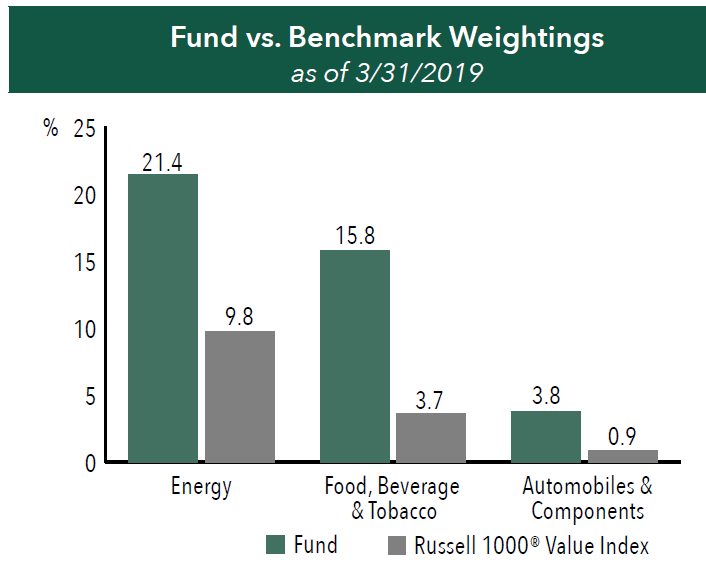

How does the current portfolio differ from its benchmark?

There are three primary industry groups where the Fund currently maintains an overweight position versus its benchmark, the Russell 1000® Value: Energy, Food, Beverage & Tobacco, and Automobiles & Components.

Performance of each of these industry groups has lagged the general market.

»In the case of Energy, where the Fund has a weighting of 21% vs. the Index weighting of 10%, weak oil prices have pushed stock

prices lower.

»In the case of Automobiles & Components, where the Fund has a weighting of 4% vs. the Index weighting of 1%, concern that auto sales may be nearing their peak, and worries over leveraged balance sheets and loss of market share have caused stock prices to lag the market.

»In the case of Food, Beverage & Tobacco, where the Fund has a weighting of 16% vs. the Index weighting of 4%, dollar strength, higher interest rates, and a shift in consumer preferences away from packaged food favorites towards new, healthier alternatives have depressed stock prices.

However, despite these headwinds, the Fund’s investments in these industry groups have maintained robust levels of profitability, and most have continued to report growth in earnings. Strong profits have allowed these companies to continue to pay healthy dividends which, combined with depressed stock prices, have produced high dividend yields.

- In this article:

- Domestic Equity

- Cornerstone Value Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Focus FundSeeking Companies with Strong Growth at Attractive Valuations

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager Brian Macauley, CFACo-Portfolio ManagerRead the Commentary

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers rely on their strategy of owning durable, well-run businesses capable of turning adversity into opportunity and adapting to macroeconomic surprises. The following Hennessy Focus Fund Commentary recaps the 2025 market and highlights areas of opportunity ahead.

-

Portfolio Perspective

Portfolio Perspective

Focus FundFrom Rate Cuts to AI: Positioning the Portfolio for Potential Opportunity

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers discuss holdings that could potentially benefit from lower rates, tariffs, and artificial intelligence (AI). The team also provides an update on AST SpaceMobile and discusses potential opportunities in select Technology and Health Care companies.

-

Company Spotlight

Company Spotlight

Focus FundO’Reilly Automotive—Revved for Growth

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the SpotlightO’Reilly Automotive is a leader in the automotive aftermarket parts industry in the U.S. The company’s scale, unique distribution infrastructure, and customer service-oriented culture should allow it to take market share in a fragmented U.S. market for years to come.