Growth in Demand, Dividends, and Earnings Presents Opportunities for Utilities

The Portfolio Managers of the Hennessy Gas Utility Fund discuss current and future natural gas and electricity demand dynamics and the increased interest in renewable energy, and they explain why utilities, with growing dividends and earnings, present an attractive investment opportunity.

-

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

How is the natural gas industry faring amidst the pandemic?

While the shutdowns and stay-at-home orders associated with the pandemic have weighed heavily on the Energy sector, demand for natural gas has proven more resilient than the demand for crude oil. While natural gas usage is down among commercial and industrial customers, much of that has been offset by residential usage, as Americans are working and schooling from home. Importantly, in some areas, residential natural gas usage can carry higher margins than commercial usage.

Overall demand for natural gas is expected to decline a modest 2% in 2020 and about 5% in 2021. Ultimately, we believe the eventual return to a normal level of economic activity should drive increased usage of natural gas. Additionally, there is growing consensus that regulators may allow utilities to recover COVID-related expenses, such as non-payment or costs to implement safety precautions, by passing costs onto ratepayers.

What is the longer-term outlook for natural gas demand?

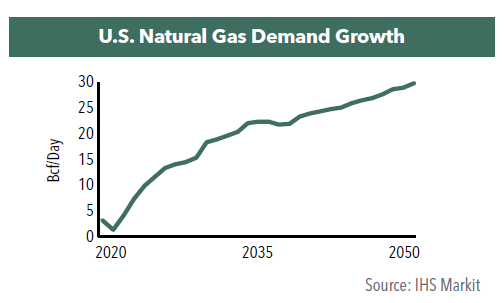

Consumption of natural gas has grown 37% over the past decade, while overall energy demand has risen only 6%. This growth has been primarily driven by the electric power generation industry switching from coal to cheaper, cleaner-burning natural gas. In the U.S., natural gas demand is expected to grow 21% by 2035 and 30% by 2050. Exports, both via LNG globally and via pipeline to Mexico, are forecast to be a significant driver of future growth.

Power sector demand is also expected to grow steadily over the next decade. We believe that increased use of electric vehicles (EVs) will increase demand for power produced, in part, by natural gas, as illustrated by California’s timeline for a transition to EVs by 2035, which will likely prompt other states and jurisdictions to announce similar directives. In our opinion, the impact of EVs on electric utilities is not fully appreciated. Transportation sector demand is also expected to grow in the next decade from its low base today with the use of compressed natural gas for trucking.

With increased interest in renewables, how is the Fund positioned to benefit?

Growing consumer preference and regulatory favor is contributing to the growing investor interest in renewable energy sources over fossil fuels. 11% of U.S. energy consumption in 2019 was from renewable sources, up from 6% in 2007. We continue to see the rapid adoption of these energy sources, with solar power consumption in 2020 up 22%, and wind-based power consumption up 11% year to date.

We believe the Fund is well positioned to capitalize on this trend with its broad-based exposure to renewables: 19 portfolio companies have exposure to solar power, 22 have exposure to wind power, and 21 have exposure to hydroelectric power generation.

Why should investors consider natural gas utilities?

Fueled by a 100+ year supply and competitive pricing, we believe natural gas will remain a compelling energy source for decades to come. The majority of U.S. natural gas needed is within our political control, and natural gas utilities are relatively insulated from major geopolitical events. The industry is enjoying a strong demand growth trajectory and a favorable regulatory environment.

In the current low rate environment, natural gas utilities offer relatively attractive dividends. However, we view these companies as much more than simply an income play given projected levels of growth in capital expenditures and earnings per share (EPS).

Companies across the Utility sector are posting long-term EPS growth of 6-8%, compared to their historical range of between 3-5%. For natural gas distribution companies, infrastructure spending can meaningfully drive earnings growth as the regulatory framework under which they operate allows them to pass on the cost of their investment plus a rate of return typically between 8 and 11%. Effectively, the more these companies invest, the more they can earn. Infrastructure spending for gas utilities is up 300% since 2007.

What is the Fund’s yield and what are your expectations for dividends going forward?

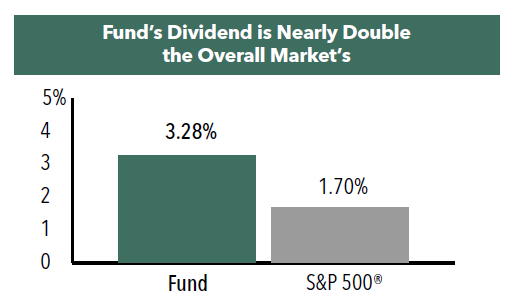

Currently, 44 out of the Fund’s 48 holdings have regularly paid a dividend. The 30-day SEC yield for the Fund (HGASX) was 3.28%, nearly double that of the S&P 500® Index as of September 30, 2020.

Our portfolio companies have raised their dividends at an average annual rate of over 5% since 2013, supported by operating income growth of 9% annually over the same period. We anticipate that the above-average period of profit growth that Utilities are currently experiencing will allow for further dividend increases.

- In this article:

- Energy

- Gas Utility Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Midstream FundPotential Natural Gas Tailwinds for Midstream Companies

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryThe following commentary highlights how recent events in Venezuela affect midstream investors, how midstream companies could benefit from interest rate cuts, rising natural gas and LNG demand, and AI-driven efficiencies, while maintaining disciplined capital allocation, strong shareholder returns, and attractive valuations.

-

Portfolio Perspective

Portfolio Perspective

Energy Transition FundThe Role of Natural Gas to Meet AI Energy Demand

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, Portfolio Manager Ben Cook and Josh Wein highlight the Fund’s 2025 outperformance, discuss the impact the events in Venezuela may have on the energy sector, and outline key 2026 Energy sector opportunities.

-

Portfolio Perspective

Portfolio Perspective

Gas Utility FundNatural Gas Utilities as a Potential Growth Story

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryWith AI-driven power demand, rising capital investments, LNG growth, and pipeline infrastructure expansion, natural gas utilities are being repositioned as potential growth stories with attractive valuations and dividends.