Utilities - Attractive Valuations with steady Earnings and Dividend Growth Potential

The Portfolio Managers of the Hennessy Gas Utility Fund discuss the higher interest rate environment and how the Fund has performed historically. They also talk about the Fund’s current composition, earnings growth, and dividends along with valuation of the Utilities sector.

-

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

How has the “higher for longer” interest rate environment affected natural gas utilities?

The “higher for longer” rate environment has affected utilities by increasing expenses and raising their cost of capital. However, utilities have the flexibility to pass these costs along to customers through rate cases and cost recovery mechanisms, but these take time. While there may be a lag, these mechanisms help them achieve their allowable return on equity.

Nevertheless, we believe investors should focus on the long-term factors that drive the Fund’s performance, including the industry’s strong fundamentals and the continued importance of natural gas and electricity.

How have the Fund’s holdings historically performed in a higher interest rate environment?

When we compare the Fund’s annual total return since its inception in 1989 to the federal funds rate, we find there has been no statistically significant correlation between the Fund’s total return and interest rate movements. Historically during periods where rates significantly increased, other fundamental factors drove performance such as increasing energy demand and earnings and dividend growth.

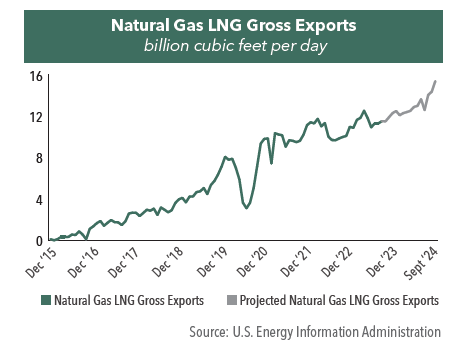

Would you please discuss the expansion of U.S. liquefied natural gas (LNG) capacity?

The U.S. has seen an incredible growth in LNG exports since exportation began in 2016, rising to become one of the top three LNG exporters in the world, along with Qatar and Australia. U.S. LNG capacity is expected to increase approximately 25% from 10.6 billion cubic feet per day (bcf/d) in 2022 to over 13.0 bcf/d by the end of 2024.

The growth in LNG capacity has been driven by increasing demand, particularly from Europe’s desire to reduce reliance on Russian energy. In addition, the price for LNG in the U.S. is significantly lower compared to other areas around the world. As of the end of October, natural gas is trading around $3.50 per million British thermal units (btu) while in Europe and Asia, it has reached around $15 to $18 per million btu, respectively.

Looking ahead, the U.S. is building more LNG export terminals, with six currently under construction. Two are scheduled to open in 2024 which will expand capacity. However, the timeline for completion can be lengthy, with some projects expected to be completed by 2030.

We note that the Fund captures a portion of the LNG market, with 5% of the portfolio invested in Cheniere Energy, a pure-play LNG exporter. Additionally, some utilities in the Fund have export facilities, contributing to the overall LNG market.

What is the current composition of the Hennessy Gas Utility Fund and how has it changed over time?

Currently, the Fund includes approximately 12% pure play natural gas utilities, 48% multi-utilities with both natural gas and electric, and 33% pipelines and LNG export energy companies. The Fund has seen a shift in composition over time, with a decrease in the percentage of natural gas utilities and an increase in the percentage of energy companies.

Another change over the years is that many of the Fund’s holdings have some exposure to renewable energy. While we expect renewables to continue to grow, it will be a decades-long process. In the meantime, we believe renewables and natural gas complement each other. Natural gas is efficient, reliable, affordable, and abundant, while renewables offer environmental advantages and are becoming more cost competitive.

Would you please discuss earnings and dividend growth of natural gas utilities?

The growth in earnings per share (EPS) of Utilities remains steady and above its long-term average. In 2022, Utilities’ EPS growth was 6% and over 2023 and 2024, EPS growth is expected to grow 5% and 9%, respectively.

Dividend growth is also solid: 47 out of 50 companies in the Hennessy Gas Utility Fund pay a dividend with an average yield of 4.6% and 4.3% growth in dividends over the past year as of 10/31/23.1

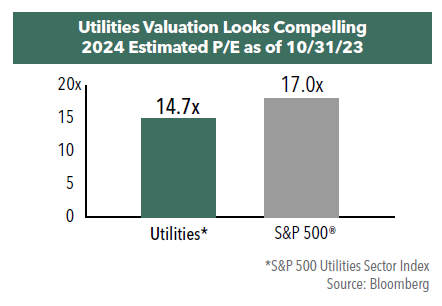

What are the valuations of Utilities compared to history and the S&P 500 Index?

Utilities currently may not be rewarded for their steady earnings growth and dividends as they are trading at a significant discount relative to history and the overall market. Relative to history, the companies in the Utilities sector traded at around 85% of the S&P 500® on a forward price-to-earnings (P/E) basis as of 10/31/23, lower than the historical average of 94% over the past 10 years.

Compared to the overall market, Utilities are trading at around 16.0x earnings for 2023 and 14.7x earnings for 2024, while the S&P 500 is trading at 18.8x earnings for 2023 and 17.0x earnings for 2024, based on forward looking estimates from Bloomberg.

Overall, the outlook for natural gas utilities is positive. The fundamentals of the companies remain strong, and the long-term demand for natural gas remains steady, especially with the increasing electrification of cars and the need for reliable energy sources.

- In this article:

- Energy

- Gas Utility Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Midstream FundPotential Natural Gas Tailwinds for Midstream Companies

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryThe following commentary highlights how recent events in Venezuela affect midstream investors, how midstream companies could benefit from interest rate cuts, rising natural gas and LNG demand, and AI-driven efficiencies, while maintaining disciplined capital allocation, strong shareholder returns, and attractive valuations.

-

Portfolio Perspective

Portfolio Perspective

Energy Transition FundThe Role of Natural Gas to Meet AI Energy Demand

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, Portfolio Manager Ben Cook and Josh Wein highlight the Fund’s 2025 outperformance, discuss the impact the events in Venezuela may have on the energy sector, and outline key 2026 Energy sector opportunities.

-

Portfolio Perspective

Portfolio Perspective

Gas Utility FundNatural Gas Utilities as a Potential Growth Story

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryWith AI-driven power demand, rising capital investments, LNG growth, and pipeline infrastructure expansion, natural gas utilities are being repositioned as potential growth stories with attractive valuations and dividends.