The Rise of Natural Gas Exports

Over the last decade, strong growth in production has allowed the U.S. to become a net exporter of natural gas. Both liquefied natural gas (LNG) exports and pipeline exports to Mexico have been growing rapidly, and significant further growth is forecast.

-

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

Key Takeaways

» The U.S. is the third largest exporter of LNG globally, trailing only Qatar and Australia in total export volumes

» Total natural gas exports increased 29% year-over-year in 2019, with LNG exports up 68%

» Global natural gas demand is expected to double to 700 million tonnes by 2040

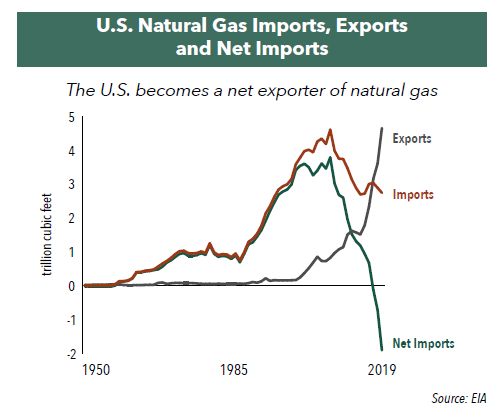

Over the past two decades, natural gas exports from the U.S. have been booming, increasing over 18-fold from 2000 to 2019. This growth has helped bring the U.S., which imported 20% of its natural gas needs back in 2007, into a position where it became a net exporter of natural gas since 2017. In fact, the U.S. has become the third-largest LNG exporter in the world behind Qatar and Australia.

The boost to exports and reduction in dependence on imports is due to rapid growth in U.S. natural gas production since 2005, driven by the discovery and exploitation of significant shale natural gas resources. Today, about 61% of natural gas exports are via pipeline, and 39% is shipped in the form of LNG. We believe there remain good prospects for growth in both channels.

LNG Exports

In 2016, the first LNG export terminal in the U.S. was opened in Louisiana. The U.S. Energy Information Administration (EIA) called the terminal “a milestone…that has put the United States in a new position in worldwide energy trade.”1 There are seven LNG export terminals operating today. Fifteen more have been approved, seven of which are under construction, and nine more are pending government approval.

The outbreak of the COVID-19 pandemic in 2020, however, has resulted in many companies pausing their LNG infrastructure spending. In addition, the impact of government-imposed closures has reduced the demand for LNG used in industrial applications, resulting in a subsequent decline in exports.

Despite these short-term challenges, the fundamental drivers of long-term demand growth remain unchanged. In fact, the EIA estimates that U.S. LNG exports set a new all-time monthly record in November 2020, surpassing pre-COVID levels, and will average in excess of 9.0 billion cubic feet per day (Bcf/d) into the first half of 2021. Global natural gas consumption is expected to double to 700 million tonnes by 2040, as the demand for imports in the quickly growing Asian and Middle Eastern markets will be supplied by imports of LNG. With China set to overtake Japan to become the leading importer of LNG, the expansion of the Panama Canal to accommodate larger LNG tankers has helped to make it easier and more cost-effective for the U.S. to become a significant supplier to high-demand Asian markets. Additionally, the market has seen increasing demand from European customers in hopes of alleviating their reliance on Russian pipeline imports, which Russia has previously used during political disputes as bargaining chips.

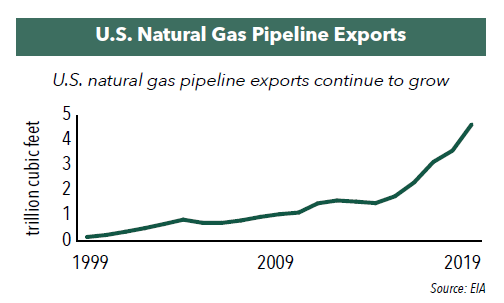

Pipeline Exports to Mexico

In addition to LNG, pipeline exports of natural gas to Mexico have also seen a tremendous increase. Exports to Mexico have grown 18-fold since 2000 and now account for over 2/3 of total pipeline exports, with the other 1/3 piped to Canada. Mexico’s national energy ministry estimates that natural gas imports from the U.S. are expected to increase by 25% by 2024, to an estimated 6.75 Bcf/d due to increased use in industrial applications and electricity generation.

Since 2016, Mexican corporations have been expanding the country’s natural gas pipeline system, and in June 2020 completed the Wahalajara system, a new system of pipelines connecting natural gas supply hubs in western Texas to major population centers in west-central Mexico including Guadalajara. While the short-term decline in demand due to COVID-19 has resulted in the pipeline operating at 10-15% capacity, the integration of new natural gas-fired generators and the scheduled completion of the Tula-Villa de Reyes pipeline into central Mexico are sure to help demand rebound to pre-covid levels.

Natural Gas Reserves

The natural gas export industry in the U.S. has significant, long-term growth potential. With the U.S. having the fourth-largest reserves globally, the EIA estimated in 2019 that the U.S. currently sits on 504.5 trillion cubic ft. of natural gas, an amount equivalent to 136 years’ worth of supply based on present production levels.

- In this article:

- Energy

- Gas Utility Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Midstream FundPotential Natural Gas Tailwinds for Midstream Companies

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryThe following commentary highlights how recent events in Venezuela affect midstream investors, how midstream companies could benefit from interest rate cuts, rising natural gas and LNG demand, and AI-driven efficiencies, while maintaining disciplined capital allocation, strong shareholder returns, and attractive valuations.

-

Portfolio Perspective

Portfolio Perspective

Energy Transition FundThe Role of Natural Gas to Meet AI Energy Demand

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, Portfolio Manager Ben Cook and Josh Wein highlight the Fund’s 2025 outperformance, discuss the impact the events in Venezuela may have on the energy sector, and outline key 2026 Energy sector opportunities.

-

Portfolio Perspective

Portfolio Perspective

Gas Utility FundNatural Gas Utilities as a Potential Growth Story

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryWith AI-driven power demand, rising capital investments, LNG growth, and pipeline infrastructure expansion, natural gas utilities are being repositioned as potential growth stories with attractive valuations and dividends.