A Focus on High-Quality Companies and Disciplined Positioning in Fixed Income

In the following commentary, the Portfolio Managers discuss portfolio changes and where they are finding opportunity in the equity and fixed income markets.

-

Stephen M. Goddard, CFAPortfolio Manager

Stephen M. Goddard, CFAPortfolio Manager -

Samuel D. Hutchings, CFAPortfolio Manager

Samuel D. Hutchings, CFAPortfolio Manager -

Gary B. Cloud, CFAPortfolio Manager

Gary B. Cloud, CFAPortfolio Manager -

Peter G. Greig, CFAPortfolio Manager

Peter G. Greig, CFAPortfolio Manager

Key Takeaways

EQUITY

» We believe the market may broaden in 2026 driven by elevated valuations of AI/tech-related names, converging earnings growth expectations, and productivity and profitability gains from companies’ adoption of AI.

» Investors could be driven to value companies due to lower valuations and improving fundamentals.

» We favor high-quality companies that generate strong free cash flow, maintain conservative balance sheets, and have a history of returning capital to shareholders.

FIXED INCOME

» The fixed income market has remained remarkably stable in recent months, despite periods of uncertainty.

» Given the uncertainty surrounding Fed policy—and the broader unknowns around tariffs and their potential economic impact—we opted to maintain a neutral duration posture throughout 2025.

» Overall, 2026 could be a year that rewards disciplined positioning and security selection —an environment that plays to our strengths.

Equity Portfolio

With market leadership driven by tech/AI in 2025, what conditions could drive a potential shift away from narrow market leadership?

We believe the market may be poised to broaden in 2026, which could potentially benefit active value-oriented large-cap managers. Some potential drivers of market broadening include:

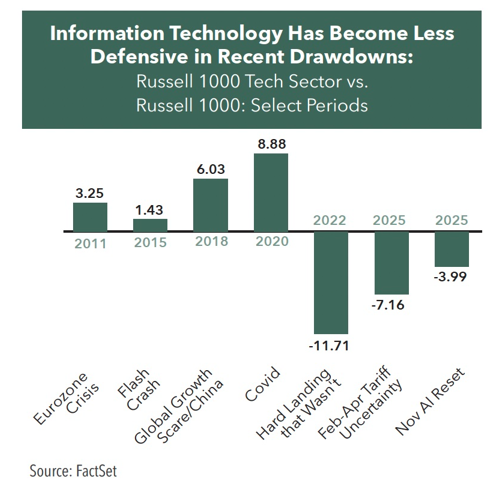

• Elevated valuations of AI/tech-related names, which makes them susceptible to multiple compression in market drawdowns or from missing lofty earnings growth expectations. While broad U.S. markets have now had 3 consecutive years of double-digit gains, the information technology sector has increasingly become less defensive in recent market drawdowns, in part due to its elevated valuation versus the market.

• Relative earnings growth expectations are converging between U.S. large cap stocks and other areas of the market. As of December 31, 2025, consensus 3-5yrs EPS growth estimates for the Russell 1000 index were 13.0%, compared to 12.3% for the Russell Midcap index, 12.5% for the Russell 2000 Index, and 10.5% for the Russell 1000 Value Index. This convergence could lead to broadening market leadership as many areas of the market are trading at steep historical discounts to large-cap stocks, despite fairly similar expected future earnings growth.

• AI adoption by companies could lead to productivity and profitability gains that benefit a wider swath of companies/industries rather than the early AI beneficiaries that have largely been confined to mega-cap, tech stocks.

What factors in 2026 could drive investors to value companies?

While rarely a catalyst in and of itself, investors could be driven to value companies due to their lower valuation relative to the historically elevated valuations of many mega-cap tech names.

Investors could be drawn to the lower valuations and higher perceived margin of safety of value companies should persistent inflation or a weakening labor market put additional pressure on stock valuations/multiples in 2026.

Conversely, should economic growth continue to be strong, bolstered by moderating inflation, deregulatory policies and the lagged effects of fiscal and monetary stimulus from 2024/2025, investors may be drawn to the improving fundamentals of many value companies, again, trading at more reasonable valuations than many growth-oriented mega-cap tech names.

Would you please discuss a recent portfolio addition and a position you exited?

In the fourth quarter, we increased our position in Republic Services (RSG) which provides increased exposure in a defensive and resilient business model. The waste management industry has lagged the broader market in 2025 due to cyclical volume weakness in construction, demolition, and the industrial sector. Despite these short-term headwinds, RSG continues to exhibit operational strength through pricing power and cost controls, which have led to stronger margins. We remain attracted to the high-quality, essential business with strong and stable cash flow generation. Recently, insiders have bought shares in the open market, which we view as an additional data point to the attractive valuation.

In August, we sold our position in global scientific technology company Bruker as the stock significantly underperformed the broader market since our purchase in 2024. Headwinds from weak pharma spending, possible cuts to National Institutes of Health and academic funding, and uncertainty due to changing tariff policy may result in further reductions to guidance. With no insider purchases or accelerated buybacks from the company, we elected to sell.

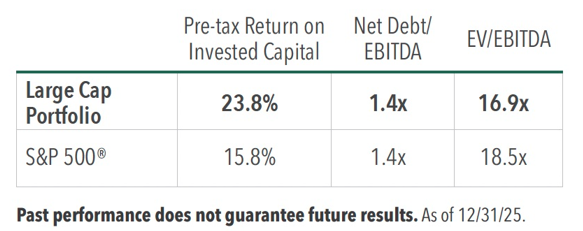

What was the portfolio’s return on invested capital, debt/EBITDA and valuation and how does it compare to the S&P 500 as of 12/31/25?

As of the end of 2025, the portfolio had a higher pre-tax return on capital of 23.8% compared to the S&P 500’s 15.8%. The equity portfolio also had a lower valuation, with an enterprise value to EBITDA of 16.9x compared to the S&P 500’s 18.5x.

Looking ahead, where do you see the most compelling opportunities, and what conditions could challenge equities in 2026?

We see the most compelling opportunities in high-quality companies with durable fundamentals, particularly those that generate strong free cash flow, maintain conservative balance sheets, and have historically returned capital to shareholders through dividends, share repurchases, and debt reduction. With valuations elevated and economic growth moderating, we believe near-term returns could be more modest, with shareholder yield comprising a meaningful portion of total returns. As the economy moves further into a late-cycle phase and monetary policy transitions from restrictive to neutral, environments like this have historically favored quality companies with durable competitive advantages. Against this backdrop, we believe the opportunity set increasingly favors high-quality companies where fundamentals matter more than multiple expansion.

Fixed Income Portfolio

Would you please summarize the fixed income market, the cuts in 2025 and your expectations for further cuts in 2026?

The fixed income market has remained remarkably stable in recent months, despite periods of uncertainty. After holding steady for the majority of the year, the Federal Reserve cut interest rates three times in 2025. These adjustments lowered the federal-funds rate by 75 basis points—from 4.25%-4.50% at the start of the year to a range of 3.50%-3.75%. Cumulatively, the Fed has reduced rates by 175 basis points since the 2024 peak of 5.25%-5.50%.

Notably, these decisions were not unanimous; dissenting votes were cast both against cutting and in favor of reductions exceeding 25 basis points. The cuts were driven by signs of a cooling labor market, marking a paradigm shift from earlier in the year when inflation—fueled by tariffs announced by the White House in April—was the primary concern.

Looking ahead, expectations generally lean toward modest additional easing. We forecast two to three cuts likely throughout 2026. A significant variable in this outlook is the appointment of a new Fed Chairman following the expiration of Jerome Powell’s term on May 15. While the board structure prevents the Chair from unilaterally assigning policy, the new appointee’s ability to influence the wider group remains to be seen.

As the Federal Reserve maintained a cautious, data-dependent stance through 2025, how did changes in rate expectations influence your fixed income positioning and risk management?

Given the uncertainty surrounding Fed policy—and the broader unknowns around tariffs and their potential economic impact—we opted to maintain a neutral duration posture throughout 2025. For us, neutral duration means staying within +/- 5% of the market in general, which allowed us to remain flexible without taking outsized interest rate risk during a period of elevated unpredictability.

This approach reflects our broader investment philosophy: duration management is not the primary driver of alpha in our process. While we do make tactical duration decisions and are thoughtful about the timing of portfolio extensions, our alpha generation is rooted in sector allocation—particularly our exposure to corporate credit—and security selection. By keeping duration close to the market, we were able to focus our risk budget on the areas where we believe we have a competitive edge, while managing rate risk in a disciplined, measured way.

What notable changes were there to the Fund’s fixed income positioning during the second half of 2025?

Our overall philosophy and outlook on the fixed income market remained consistent throughout the second half of 2025, so the changes we made were incremental rather than strategic shifts.

On the duration side, as interest rates moved toward the higher end of their range, we took advantage of those opportunities to extend the portfolio. This is a natural part of maintaining our neutral duration stance—while the market’s duration stays relatively stable as new issues enter and short-dated bonds roll off, our portfolio’s duration drifts lower each month as the bonds we hold approach maturity. Periodic extensions are necessary to keep pace with the market, and we prefer to execute those when we view rate levels as attractive.

On the credit side, we used the period to improve diversification within the portfolio as certain credit positions had grown large as a percentage of the overall portfolio. We trimmed some of these more concentrated positions and redeployed into a broader set of corporate issuers, reducing single-name risk while maintaining our overall credit exposure.

How did your view of the yield curve evolve over the course of 2025, and where do you currently see the most attractive risk-adjusted opportunities?

Coming into 2025, our expectation was for yields to decline in a more meaningful way than what occurred—particularly on the longer end of the curve. However, that view shifted following the tariff announcements in the spring. The resulting inflation concerns kept long-term rates elevated. As more data emerged throughout the year, we shifted to expect a more meaningful curve steepener, which occurred. We expect that trend to continue, albeit more modestly, into 2026.

Our current view is that as the Fed delivers additional rate cuts, the front end of the curve will trend lower in yields, while the long end will likely remain anchored near the recent trading range. If that plays out, the return profile for longer-duration bonds will be fairly straightforward: limited price movement, with investors earning close to their starting yield. The front end offers modestly more upside from a price perspective, but there are offsets—lower starting yields due to the positively sloped curve, and lower duration, which mutes the price impact of any rate moves.

While the front end may outperform on a total return basis, the margin is unlikely to be significant. In that environment, we see the most attractive risk-adjusted opportunities in the intermediate part of the curve, where we believe you can capture reasonable yield without taking excessive duration risk.

What is the fixed income portfolio’s duration profile and yield-to-worst as of 12/31/25?

The duration profile of the portfolio was at the higher end of our neutral policy at year-end. The portfolio had a duration of 3.906 and the overall yield-to-worst was 4.05%.

Would you please provide your fixed income outlook for 2026?

We enter 2026 cautiously optimistic about the fixed income landscape. Our base case is for above-trend GDP growth, with the first half of the year likely outpacing the second half as fiscal tailwinds—including One Big Beautiful Bill Act related tax stimulus—along with events like the World Cup and America 250 celebrations provide a boost to economic activity. While these dynamics have the potential to be inflationary, we expect inflation to drift modestly lower as the year progresses.

From a rates perspective, we continue to expect the yield curve to steepen. As the Fed delivers additional cuts, the front end should move lower, while the long end remains relatively anchored. For investors, this means the opportunity on longer-duration bonds will largely be from yield, rather than price appreciation. The front end offers some price upside, though the lower starting yields and reduced duration sensitivity limit the total return advantage.

On the credit side, spreads remain tight, and we wouldn’t be surprised to see modest widening over the course of the year. That said, we still believe corporate credit could outperform Treasuries on a total return basis, as the additional carry more than compensates for the spread risk.

Overall, we see 2026 as a year that rewards disciplined positioning and security selection over aggressive rate bets—an environment that plays to our strengths.

- In this article:

- Multi Asset

- Equity and Income Fund

You might also like

-

Fund Commentary

Fund Commentary

Equity and Income FundNavigating Volatility in Equities and Fixed Income

Stephen M. Goddard, CFAPortfolio Manager

Samuel D. Hutchings, CFAPortfolio Manager

Gary B. Cloud, CFAPortfolio Manager J. Brian Campbell, CFAPortfolio ManagerRead the Commentary

J. Brian Campbell, CFAPortfolio ManagerRead the CommentaryThe Portfolio Managers of the Hennessy Equity and Income Fund discuss how they navigated the volatile markets during the first half of the year, outlining portfolio changes and areas where they are uncovering opportunities.

-

Fund Commentary

Fund Commentary

Equity and Income FundAn Opportunistic Balance of High-Quality Stocks and Investment Grade Bonds

Stephen M. Goddard, CFAPortfolio Manager

Samuel D. Hutchings, CFAPortfolio Manager

Gary B. Cloud, CFAPortfolio Manager

Peter G. Greig, CFAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the actively managed Hennessy Equity and Income Fund provide their perspective on investing in high-quality companies and investment grade bonds in 2025.

-

Fund Commentary

Fund Commentary

Equity and Income FundA Comprehensive Market Overview and Update On the Fund's Positioning

Stephen M. Goddard, CFAPortfolio Manager

Gary B. Cloud, CFAPortfolio Manager

J. Brian Campbell, CFAPortfolio Manager

Peter G. Greig, CFAPortfolio Manager

Samuel D. Hutchings, CFAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the actively managed Hennessy Equity and Income Fund (HEIFX/HEIIX) share their perspective on the equity and fixed income markets, a new equity holding, where on the yield curve they are finding opportunity, and their outlook for the remainder of 2024.