Mitsubishi UFJ Financial Group

Amid a tough banking environment over the past few years, many Japanese banks streamlined their operations to achieve record profits. In addition, they are poised to increase their profitability due to potential rate increases. Mitsubishi UFJ Financial Group looks particularly attractive in today’s environment.

-

Masakazu Takeda, CFA, CMAPortfolio Manager

Masakazu Takeda, CFA, CMAPortfolio Manager -

Angus Lee, CFAPortfolio Manager

Angus Lee, CFAPortfolio Manager

The Japanese Banking Industry

Deposit, lending, and settlement services provided by banks are indispensable to consumers and businesses. In developed countries, the customer base extends to almost all consumers and corporations, hence the market size is enormous.

To operate these businesses smoothly and efficiently, banks are capital intensive and require a large number of human resources, and fixed assets such as branch networks and information technology (IT) systems. Also, because they play a critical role in a country’s economy, banks must obtain licenses from the financial regulatory authorities, creating a high barrier to entry.

Among existing banks, the competition is fierce because it is difficult to differentiate deposit and lending services from those of other banks. For this reason, the return on invested capital of the banking industry is generally lower than that of other industries. To achieve high return on equity (ROE), leverage is needed. As such, the banks’ balance sheets are highly leveraged, and a management misstep can magnify the negative impact on profitability.

The following are the criteria we use to select attractive banks as an investor. In our view, these are the same investment criteria used by renowned investor Warren Buffett:

• Deposit franchise: Whether the bank has a brand power that allows people to deposit their money with confidence. If a bank has a strong brand backed by safety and convenience, it can raise funds at a low cost.

• Lending discipline: Whether they are conducting sound lending operations. After a loan is made, it is rare for it to become a bad debt right away while interest income is generated immediately. For this reason, bank management are often tempted to increase short-term profits and end up making risky loans. Importance is placed on whether they are properly conducting disciplined lending and applying interest rates that match the credit risk of the borrower.

• Cost controls: Whether they have excellent cost management abilities. In the banking industry, where profitability is not necessarily high due to intense competition among existing players, a low-cost mindset is paramount.

Mitsubishi UFJ Financial Group

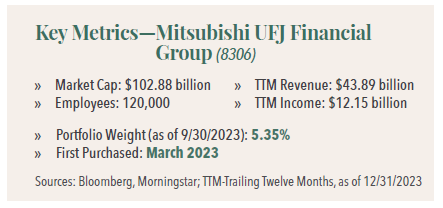

Mitsubishi UFJ Financial Group (MUFG) meets the above criteria. MUFG is one of the three largest mega-banks in Japan, boasting the largest scale in the country. It has 214 trillion yen ($1.4tn) in deposits, 110 trillion yen ($735bn) in loan assets, about 120,000 employees, 34 million individual customers, 1.1 million corporate customers, 436 domestic bases, and about 1,600 overseas bases.1

Compared to Japanese regional banks, MUFG has a strong overseas presence. While the global expansion of foreign banks has been rife with challenges historically (think Citi Bank, Standard Chartered, HSBC, Credit Suisse, etc.), MUFG’s overseas profits account for nearly half of the total. In addition, it holds a 22% stake in Morgan Stanley as an affiliate. Back in 2008, MUFG swooped in to invest in the U.S. investment bank at the height of the global financial crisis. This decision is acclaimed as one of the most successful deals in merger and acquisition (M&A) history. Today, Morgan Stanley contributes over 300 billion yen ($2bn) in equity income with an investment return of 12% (equity income/MUFG’s share of book value), exceeding the average ROE of MUFG as a whole.2

Normalization of Domestic Interest Rates

To make a case for MUFG as a compelling investment, we cannot avoid discussing the potential for profit growth based on the outlook for interest rates. This is because the current low-interest rate environment results in too low profitability for Japanese banks.

MUFG has the largest asset size among Japanese banks. As of the end of March 2023, it had total assets of 387 trillion yen ($2.6tn), rivalling HSBC and about 80% the size of JPMorgan, making it one of the largest banks in the world. On the other hand, in terms of return on assets (ROA)—net income/total assets—HSBC and JPMorgan each earn net profit equivalent to 0.5% and 1.0% of total assets, respectively, while MUFG only earns 0.3%. This is typical of Japanese banks.

One of the reasons for the low ROA is the large amount of money deposited with the Bank of Japan (BOJ). These deposits do not earn interest (some even have negative interest rates), so they can be considered “dead money” on the balance sheet. In the case of MUFG, the BOJ account deposits amount to about 80 trillion yen ($534bn), or about 20% of total assets.

Signs of rising interest rates have emerged recently, spurred by the first domestic inflation in nearly two decades. In Japan, where negative interest rates have been the norm, it might be more apt to say that the country is ‘moving towards normalization.’ This shift is a positive development for the future of banking. The difference in ROA between MUFG and HSBC may appear narrow (MUFG 0.3% vs. HSBC 0.5%). However, given the scale of total assets (approximately 90% of which are assets likely to benefit from rising interest rates), even a minor increase in interest rates can yield substantial profits.

For example, if half of MUFG’s BOJ account deposits were invested in the Japanese Government Bond (JGB) market or lent out at a yield of 50 basis points (bps), the effect on the bank’s net profit would be an increase of 140 billion yen/$935mn. If all of the BOJ account deposits were to earn a 1% yield, the bank’s net profit increase would increase 50% compared to FY22.

In a world with interest rates, we can also expect an improvement in loan spreads on existing lending assets. For example, if the yield on lending goes up by 50bps, the bank’s domestic loan balance of 67 trillion yen/$447bn (as of FY22) will see an increase of 230 billion yen ($1.5bn) in net profit, and if it improves by 100bps, the increase would be nearly 500 billion yen ($3bn). Combined with the effect of shifting BOJ account deposits, the total net profit could expand by more than 1 trillion yen ($6.7bn). In other words, the profit would almost double from the current level.

For a bank’s financial performance, the nominal interest rate is what matters. Theoretically, if the inflation runs higher than expected, the real interest rate will decrease leaving the current ultraloose monetary policy framework intact, and there will be room for the nominal interest rate to rise further so long as the economic growth remains on track. Therefore, it is entirely possible to conjure up a scenario in which the bank’s performance can benefit from a rate expansion of more than 1%.

Banks’ fee income businesses will also enjoy growth. For example, in the derivatives business, there will be an increase in the need to fix borrowing rates through interest rate swaps, or their securities subsidiaries may see an increase in demand for corporate bond issuance. On the back of rate normalization, there may be more M&A activities, leading to higher investment banking-related fees as well.

Neutral Interest Rate of Japan

Is the above assumption of rising interest rates valid? At a minimum, we think the assumption is not unreasonable. Consider current trends in the Japanese economy:

• Core consumer price index (CPI) has been trending above 3% since Sept 2022

• The BOJ’s inflation target (“price stability target”) is 2%

• The output gap in the Japanese economy has improved to near zero

• Inflation expectations have been rising to 1.20+% as shown by Japanese Breakeven 10 year (BEI) up from 0.2% in 2019

• Factors such as Japan’s labor costs causing inflation are structural, not transitory

• The potential growth rate of the Japanese economy is estimated to be at least 0.5%

It would not be surprising if the neutral interest rate in Japan rose to around 2%. Therefore, the above scenario of a 1% rate improvement is not all that unrealistic in our view.

One thing that can be said about domestic inflation is that Japan has entered an era of labor shortage. From a demographic perspective, the decline of Japan’s total population since around 2008 has been largely offset by the extension of the employment period for the elderly and the increase in the labor participation rate of women, maintaining a flat trend in the total labor force for the past 10 years. However, the effect of these is finally reaching its limit. Unless a radical policy of accepting immigrants from overseas is discussed, it is almost certain that there will be a chronic labor shortage. Companies will have no choice but to raise wages to secure manpower. Also, improvements in productivity through automation and other means are indispensable. This implies a rise in capital investment trends in Japan going forward, which is expected to lead to an increase in the demand for funds. For these reasons, the likelihood of interest hikes is becoming higher than ever.

Potential Risks of Higher Interest Rates

What could be the potential risk of higher interest rates to the Japanese economy and the banks, or the factors that could suppress the rise in interest rates?

1. The impact on corporate interest payment burden. In Japan, for large corporations with a capital of more than 1 billion yen ($6.7mn), the aggregate operating profit (OP) for FY22 was 37.7 trillion yen ($252bn), while the interest paid was 3.7 trillion yen/$25bn (hence borrowing rate is about 1%).3 Therefore, the rise in borrowing costs from the impact of rate hikes should

be manageable. For small businesses with a capital of less than 50 million yen ($334k), the aggregate OP was 7.7 trillion yen ($51bn), while the interest paid reached 2.3 trillion yen ($15bn). If interest rates rise, many inefficient small businesses and most “zombie companies” will likely come under pressure, a potential headwind for the economy that Japan must overcome through government policy support and corporate self-determination as well as own efforts. It may be painful, but we believe that this is essential to put a definitive end to deflation.

2. In the household sector, housing loans are a concern. In Japan, the proportion of variable-rate housing loans is over 70%, which is high compared to the U.S.4 If interest rates start to rise significantly, households may face difficulties. However, given the average application size of new housing loans in Japan is between 25 and 30 million yen ($167–200k), we would estimate that the average balance of typical housing loans being repaid is less than 20 million yen ($134k).5 Based on this assumption, if the mortgage rates rise by 1%, the increase in monthly interest payments would be around 15,000 yen ($100). This is manageable for households if companies can achieve continuous wage increases.

3. Risk in the Japanese Government Bond (JGB) Market. The BOJ’s current account deposits from domestic financial institutions exceed 500 trillion yen ($3.3tn) in total, so once this “dead money” is freed up, the potential demand for JGBs can be massive, in the order of several hundred trillion yen. On the supply side, the new JGB issuance is estimated to be about 35 trillion yen ($234bn) per year, and if we assume that the BOJ does not roll over the maturing JGBs it holds, it is about 65 trillion yen ($434bn) per year, totaling about 100 trillion yen ($668bn) that Japanese commercial banks can buy.6 Buying demand can easily outstrip supply, which may suppress long-term yields, and bank earnings may not improve as much as expected as a result.

For banks who are the JGB buyers, there is also concern that their bond holdings will suffer unrealized losses with rises in interest rates. That said, the duration of MUFG’s bond portfolio (total of 37 trillion yen/$247bn, of which 13.5 trillion yen/$90bn is held-to-maturity) is only 1.5 years as of the end of FY22. Thus, it is entirely possible to see a move by the bank to gradually increase the purchase of JGBs and even add long-dated bonds, which will give them higher returns.

As for the bank’s cost of funds, banks may be forced to raise deposit interest rates. However, most if not all Japanese commercial banks are awash with deposits that far exceed loan demand, so we think that the risk of mega banks having to significantly raise deposit rates to secure funds is small.

Lastly, there are other possible side effects. In the event the BOJ finally discontinues the negative rate policy and raises the short-term rates by 1-2%, or the long yields rise by 1-2%, then the central bank’s equity could fall into negative due to a assets and liabilities management (ALM) mismatch. The probability of developing a major problem is extremely low in our view, considering that Japan can print money in its currency, that the country as a whole is one of the largest net creditor nations, and that the credibility of the BOJ is unlikely to be lost immediately.

Stock Price Valuation

Although Japanese bank stocks (including MUFG) have risen since the beginning of 2023, they remain inexpensive relative to global peers. The market cap to total assets ratio of MUFG is only 4%, compared to 13% for JPMorgan and 6% for HSBC. If MUFG were valued at the same level as HSBC, there would be a 50% upside to its market cap.

In terms of profitability, it seems at least directionally that the net interest margin (NIM) and ROA of Japanese banks, including MUFG, are going to improve from low levels. On the other hand, U.S. banks like JPMorgan already have high NIMs, so their upside appears limited. Rather, considering the U.S. economic outlook and upcoming more stringent capital requirement rules, there will be downward pressure on ROA.

Margin of Safety

Finally, even if the premise of rising interest rates does not materialize, MUFG shareholders should be rewarded with a decent return thanks to high dividend yields and continuous share repurchases.

MUFG has long aimed to consistently earn over 1 trillion yen ($6.7bn) in net income (attributable to the parent company). This target has been exceeded in the last two fiscal years, and President Kamezawa has recently commented that this objective is largely achieved. As for the dividend payout ratio, the policy is to progressively raise it towards 40% (35.3% in FY22, 37.9% planned for FY23). This means that the total amount of dividends should be at least 400 billion yen ($2.7bn).

In addition, MUFG will flexibly buy back its shares and plans to cancel up to 5% of the outstanding shares, provided that the Common Equity Tier 1 (CET1) ratio is within the target range of 9.5% to 10% (10.3% as of FY22). Given that the bank already has sufficient footprints in the U.S., Europe and Asia compared to its rival mega banks SMFG and Mizuho, making it unlikely to require large amounts of funds, their shareholder return policy looks credible. If the size of the Tier 1 capital as a percentage of risk assets can be maintained at the current levels, the bank can buy back up to 500 billion yen ($3.3bn) of shares per year. As such, MUFG shareholders can expect a total return of close to 1 trillion yen ($6.7bn) per year. We believe the TSR of 6% at the present market cap will support the downside of the stock price.

Like the mega insurance groups, we hold in our portfolio, the fact that they hold a large amount of “policy shareholdings” is also a powerful weapon. For example, MUFG holds such shares worth 2.5 trillion yen ($16.7bn) at market value as of FY22. By selling these shares, they can use them for their share buybacks as well as paying higher dividends.

All three megabanks, including MUFG, have a price to book ratio of less than 1x (PBR1x). Continuous share buybacks and dividend increases can be very advantageous for shareholders, particularly in situations where the stock price level is low, the impact of a dividend increase can be greater. In share buybacks, more shares can be bought, resulting in higher earnings per share for shareholders. What’s more, when the share price is less than PBR1x, these actions can increase the per-share book value. In other words, if the stock price does not change, the attractiveness of the valuation becomes even more pronounced.

- In this article:

- Japan

- Japan Fund

You might also like

-

Investment Idea

Investment IdeaCompelling Valuations in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager Tadahiro Fujimura, CFA, CMAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager Takenari Okumura, CMAPortfolio ManagerRead the Investment Idea

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaJapanese equities are currently trading at compelling valuation levels compared to other developed equity markets around the world and relative to their own historical averages. We believe the Japanese market deserves a closer look.

-

Investment Idea

Investment IdeaWhy Active Matters When Investing in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaWhen investing in Japanese businesses, we believe it is imperative to select a manager who is immersed in the culture and can perform in-depth, company-specific research to build a concentrated portfolio of Japanese companies that can outperform a benchmark and weather volatility.

-

Company Spotlight

Company Spotlight

Japan FundBerkshire Hathaway’s Stake in Tokio Marine Highlights the Appeal of Japanese Insurers

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio ManagerRead the SpotlightTokio Marine is Japan’s largest general insurance group with a solid track record in the domestic market and an expanding overseas business. Tokio Marine is one of three Japanese insurers that has significant market share and enjoys high profitability and strong pricing power due to industry consolidation—qualities Berkshire Hathaway appears to have noticed.