High Profitability and Attractive Valuations-A Powerful Combination

In the following commentary, the Portfolio Managers of the Hennessy Cornerstone Large Growth Fund discuss the Fund’s quantitative investment process and how it drives the Fund’s sector and industry positioning.

-

Neil J. HennessyChief Market Strategist and Portfolio Manager

Neil J. HennessyChief Market Strategist and Portfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

What is the Hennessy Cornerstone Large Growth Fund’s investment strategy?

The Fund utilizes a formula-based approach to build a portfolio of attractively valued, highly profitable, larger-cap companies. In essence, the strategy seeks high quality, high return companies that may be being overlooked by investors.

From the universe of stocks in the S&P Capital IQ Database, the Fund selects the 50 stocks with the highest one-year return on total capital which also meet the following criteria, in the specified order:

» Above-average market capitalization

» Price-to-cash flow ratio less than the median of the remaining securities

» Positive total capital

Why does the Fund use these screening criteria?

Larger market capitalization companies tend to be well-established leaders in their industries with long, successful track records and solid profitability.

A low price-to-cash flow ratio can be a good indicator of attractive stock valuation. Positive cash flow tends to be associated with companies with profitable business models.

The use of positive total capital as a screening criterion helps the Fund avoid financially weaker companies.

Why does the formula select stocks with the highest one-year return on total capital?

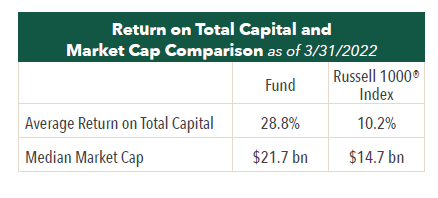

From among the companies that meet the screening criteria, the Fund selects the 50 with the highest one-year return on total capital. We believe return on capital is an excellent measure of a company’s profitability and is often associated with able management, high barriers to entry, and other favorable factors. As a result, we believe this measure can help uncover stocks with the potential to outperform the market.

How does the Fund seek to provide a return to investors?

We believe the Fund’s investments present the potential for capital appreciation when and if market sentiment changes and their valuations rise. Strong profitability also has the potential to lead to earnings growth, which could also drive capital appreciation.

How often does the Fund rebalance its portfolio?

The universe of stocks is re-screened and the portfolio is rebalanced annually, generally in the winter. Holdings are weighted equally by dollar amount with 2% of the Fund’s assets invested in each.

How does the Fund’s portfolio differ from its benchmark?

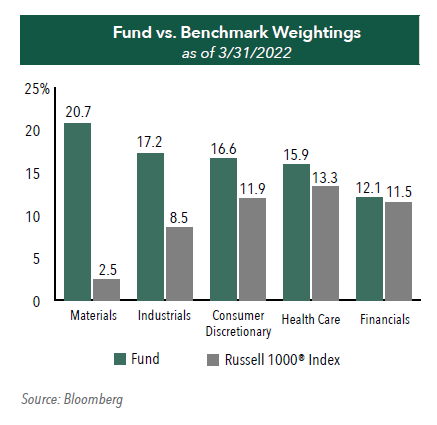

The Fund currently maintains significant overweight positions versus its benchmark, the Russell 1000® Index, in the Materials, Industrials, and Consumer Discretionary sectors.

The Fund’s largest sector weighting is Materials and is comprised of ten large cap stocks in the steel, aluminum, copper, paper, and chemicals sub-industries. With a potential rebound in the U.S. and global manufacturing economy, we believe that many of these companies could profit from increased demand for their products and higher inflation. Similarly, certain Industrials, including those in freight and shipping, building products, and industrial machinery, could experience a period of increased revenues and profitability as global economic demand increases. These more cyclical Materials and Industrials are balanced by the Fund’s positions in less cyclical, more defensive sectors such as Health Care and Financials. Many financial companies could benefit from a rising rate environment as the Federal Reserve has already begun a potentially prolonged period of interest rate hikes.

Of note, the Fund is significantly underweight the Information Technology sector compared to its primary benchmark. We attribute this to the generally higher valuations placed on many of these companies, with price-to-cash flows typically higher than the median of the investable universe and therefore excluded from the Fund.

- In this article:

- Domestic Equity

- Cornerstone Large Growth Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Focus FundSeeking Companies with Strong Growth at Attractive Valuations

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager Brian Macauley, CFACo-Portfolio ManagerRead the Commentary

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers rely on their strategy of owning durable, well-run businesses capable of turning adversity into opportunity and adapting to macroeconomic surprises. The following Hennessy Focus Fund Commentary recaps the 2025 market and highlights areas of opportunity ahead.

-

Portfolio Perspective

Portfolio Perspective

Focus FundFrom Rate Cuts to AI: Positioning the Portfolio for Potential Opportunity

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers discuss holdings that could potentially benefit from lower rates, tariffs, and artificial intelligence (AI). The team also provides an update on AST SpaceMobile and discusses potential opportunities in select Technology and Health Care companies.

-

Company Spotlight

Company Spotlight

Focus FundO’Reilly Automotive—Revved for Growth

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the SpotlightO’Reilly Automotive is a leader in the automotive aftermarket parts industry in the U.S. The company’s scale, unique distribution infrastructure, and customer service-oriented culture should allow it to take market share in a fragmented U.S. market for years to come.