Portfolio Drivers: Mid-Caps, Energy Demand, and Consumer Spending

Portfolio Managers Ryan Kelley and Josh Wein review the Fund’s investment strategy and discuss the Fund’s most recent rebalance and changes in the portfolio composition. They also highlight the fundamental drivers of select sectors within the portfolio.

-

Neil J. HennessyChief Market Strategist and Portfolio Manager

Neil J. HennessyChief Market Strategist and Portfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

What is the Fund’s investment strategy?

The Cornerstone Mid Cap 30 Fund utilizes a quantitative formula to select 30 domestic, mid-cap stocks with market capitalizations between $1 and $10 billion that exhibit both value and momentum characteristics. The formula selects stocks with higher year-over-year earnings, positive stock price appreciation, and lower price-to-sales ratios. The universe of mid-cap stocks is screened using these criteria, and the portfolio is rebalanced annually, generally in the fall. Each stock is equally weighted at approximately 3.3% of the portfolio at the beginning of the rebalance, although stock price movements can cause relative weights to change over time.

Would you please discuss sector weightings and the themes supporting those sectors?

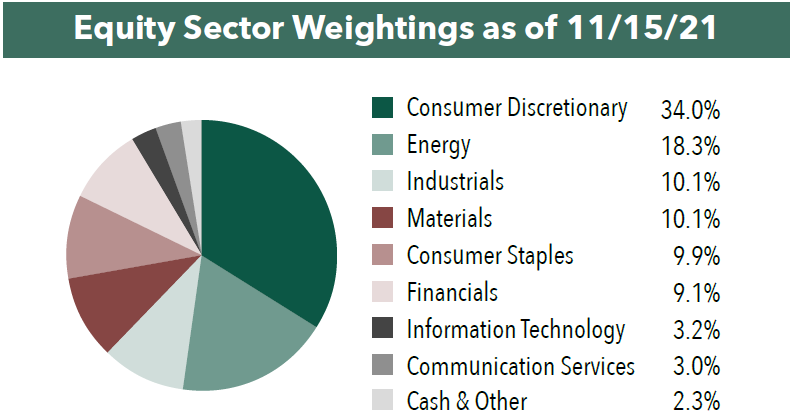

Following the most recent annual rebalance, the Fund’s holdings include stocks representing eight of the 11 GICS sectors; there are no holdings in the Health Care, Real Estate, or Utilities sectors. Like last year’s portfolio, the largest sector exposure is Consumer Discretionary with 10 out of 30 holdings. The Fund’s second-largest sector is Energy, with six holdings overall. The largest percentage drop in concentration, decreasing from two holdings to none, occurred in the Health Care sector. While the Fund overall remains a highly concentrated, focused portfolio of only 30 mid-cap equities, we view this year’s portfolio as one of the more diversified in many years given that it has three or more stocks in six of the 11 GICS sectors.

Compared to the Russell Midcap® Index, the Fund continues to have a substantial overweight position in consumer-related stocks, both Consumer Discretionary and Consumer Staples, as well as Energy. As the economy continues to reopen from the pandemic, we believe that increases in consumption, coupled with relief in supply chain bottlenecks, may drive higher growth in earnings and positive stock price performance for many of the Fund’s consumer-related holdings. Additionally, with persistent higher energy prices and continued consumer, industrial, and commercial demand, we believe many of the Fund’s investments in the Energy sector could benefit.

Is there a common investment theme in the current portfolio?

The Fund has maintained a higher concentration of Consumer Discretionary stocks than its primary benchmark, the Russell® Midcap Index, and this year is no different. Thematically, we believe many of the holdings would do very well in an increasing consumer spending environment, particularly spending related to auto sales/parts/service, specialty retail, and apparel. With the potential for continued economic recovery in 2022 and a return to in-person shopping, we would expect retailers to benefit. Additionally, any improvement in supply chain issues could benefit transportation, trucking, and distribution holdings in the Fund.

Another common investment theme within this year’s portfolio is related to energy. The Fund has holdings up and down the supply chain, including exploration and production companies, equipment manufacturers, pipeline companies, and refineries. The surge in energy prices and increase in demand due to the continued reopening of the economy have benefited many energy companies, a trend which we believe should continue into 2022 as growth in production should continue to lag increasing demand as worldwide supply constraints persist.

What is the median market capitalization of the Fund’s holdings following the most recent rebalance?

The Fund selects its holdings from a universe of mid-cap stocks with market capitalizations ranging from $1 billion to $10 billion. As of November 15, 2021, the median market cap of the Fund was $5.8 billion, down from last year’s $7.1 billion at the end of the rebalance in 2020 and about half that of the median market cap of the Russell® Midcap Index. We believe mid-caps offer untapped potential and that investors may be surprised to learn that mid-cap stocks have outperformed both small- and large-cap stocks over the past twenty-year period with less risk than small-cap stocks.

Would you please discuss the relative valuation of the Fund’s holdings compared with the benchmark?

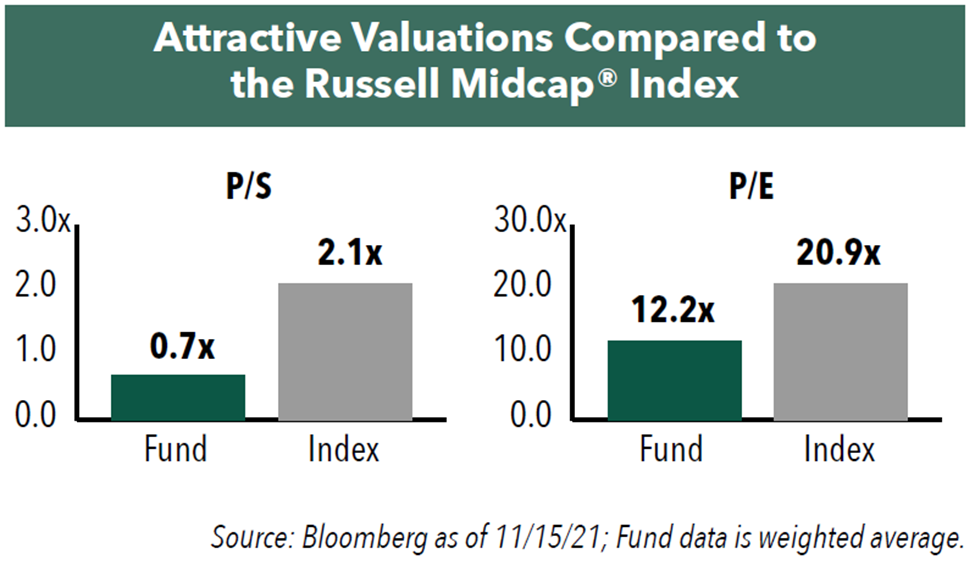

Attractive valuation is an important criterion in the Fund’s stock selection process. The Fund uses price-to-sales as its primary valuation metric because it is a simple metric, can be universally applied, and is difficult for companies to manipulate. The Fund selects stocks with a price-to-sales ratio below 1.5x. The weighted average price-to-sales ratio of the portfolio was just 0.7x as of November 15, 2021, compared to 2.1x for its benchmark index, the Russell® Midcap Index.

The Fund’s holdings are also trading at a significant discount in terms of price-to-earnings. The Fund’s weighted average price-to-earnings ratio was 12.2x as of November 15, 2021, versus 20.9x for its benchmark index.

- In this article:

- Domestic Equity

- Cornerstone Mid Cap 30 Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Focus FundSeeking Companies with Strong Growth at Attractive Valuations

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager Brian Macauley, CFACo-Portfolio ManagerRead the Commentary

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers rely on their strategy of owning durable, well-run businesses capable of turning adversity into opportunity and adapting to macroeconomic surprises. The following Hennessy Focus Fund Commentary recaps the 2025 market and highlights areas of opportunity ahead.

-

Portfolio Perspective

Portfolio Perspective

Focus FundFrom Rate Cuts to AI: Positioning the Portfolio for Potential Opportunity

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers discuss holdings that could potentially benefit from lower rates, tariffs, and artificial intelligence (AI). The team also provides an update on AST SpaceMobile and discusses potential opportunities in select Technology and Health Care companies.

-

Company Spotlight

Company Spotlight

Focus FundO’Reilly Automotive—Revved for Growth

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the SpotlightO’Reilly Automotive is a leader in the automotive aftermarket parts industry in the U.S. The company’s scale, unique distribution infrastructure, and customer service-oriented culture should allow it to take market share in a fragmented U.S. market for years to come.