A Focus on Dividend Yield to Uncover Value

In the following commentary, the Portfolio Managers of the Hennessy Cornerstone Value Fund discuss the Fund’s formula-based investment strategy and how it drives the Fund’s sector and industry positioning.

-

Neil J. HennessyChief Market Strategist and Portfolio Manager

Neil J. HennessyChief Market Strategist and Portfolio Manager -

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

What is the Hennessy Cornerstone Value Fund’s investment strategy?

The Fund utilizes a formula-based approach to build a portfolio of potentially undervalued, profitable, large-cap companies. From the universe of stocks in the S&P Capital IQ Database (excluding Utilities), the Fund selects 50 stocks with the highest dividend yield which also meet the following criteria:

» Above-average market capitalization

» Above-average number of shares outstanding

» Trailing 12-month sales 50% greater than average

» Above-average cash flow

Why does the Fund use these screening criteria?

These criteria help the Fund find companies that are large, profitable and able to pay a healthy dividend.

- Large market capitalizations tend to be associated with companies that are well-established leaders in their industries, with long successful track records and solid profitability.

- A large revenue base tends to be associated with companies that have high market shares or that have diversified successfully.

- Above average cash flow identifies companies with strongly profitable business models, possibly generating excess cash flow, which may be returned to shareholders in the form of a dividend.

Why does the formula select stocks with the highest average dividend yield?

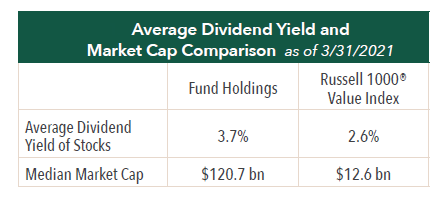

From among the companies that have passed the screening criteria, the Fund then selects the 50 with the highest average dividend yield. As high average dividend yield can be a good indicator of a low stock valuation, this ranking criteria helps uncover potentially undervalued companies.

How does the Fund seek to provide a return to investors?

We believe the combination of profitability and value offers investors an opportunity to earn a return in two ways. In our view, the Fund’s investments offer the potential for capital appreciation if and when market sentiment changes and their valuations rise. Investors in the Fund are also “paid to wait,” potentially rewarded with a steady income stream from the dividends.

How often does the Fund rebalance its portfolio?

The universe of stocks is re-screened and the portfolio is rebalanced annually, generally in the winter. Holdings are weighted equally by dollar amount with 2% of the Fund’s assets invested in each.

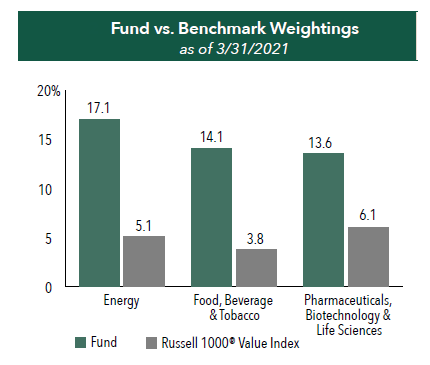

How does the current portfolio differ from its benchmark?

The Fund maintains an overweight position versus its benchmark, the Russell 1000® Value, in Energy, in Food, Beverage & Tobacco, and in Pharmaceuticals, Biotechnology & Life Sciences.

The performance of the Energy industry group has outperformed the general market, while the Food, Beverage & Tobacco and Pharmaceuticals, Biotechnology & Life Sciences industry groups have lagged the market over the last year.

» In the case of Energy, where the Fund has a weighting of 17% vs. the Index weighting of 5%, the prospect of a sharp global economic rebound has pushed stock prices higher.

» In the case of Food, Beverage & Tobacco, where the Fund has a weighting of 14% vs. the Index weighting of 4%, while sales remained relatively robust over the last year, the shares of these companies did not keep pace with the broader market as the large technology weighting in major indices propelled them higher.

» In the case of Pharmaceuticals, Biotechnology & Life Sciences, where the Fund has a weighting of 14% vs. the Index weighting of 6%, the share prices of these companies lagged the market due to the continuing effects of a shift in health care spending due to the pandemic.

The Fund’s investments in these industry groups have maintained robust levels of profitability, and many have continued to report growth in earnings. Strong profits have allowed these companies to continue to pay healthy dividends.

- In this article:

- Domestic Equity

- Cornerstone Value Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Focus FundSeeking Companies with Strong Growth at Attractive Valuations

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager Brian Macauley, CFACo-Portfolio ManagerRead the Commentary

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers rely on their strategy of owning durable, well-run businesses capable of turning adversity into opportunity and adapting to macroeconomic surprises. The following Hennessy Focus Fund Commentary recaps the 2025 market and highlights areas of opportunity ahead.

-

Portfolio Perspective

Portfolio Perspective

Focus FundFrom Rate Cuts to AI: Positioning the Portfolio for Potential Opportunity

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryThe Portfolio Managers discuss holdings that could potentially benefit from lower rates, tariffs, and artificial intelligence (AI). The team also provides an update on AST SpaceMobile and discusses potential opportunities in select Technology and Health Care companies.

-

Company Spotlight

Company Spotlight

Focus FundO’Reilly Automotive—Revved for Growth

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the SpotlightO’Reilly Automotive is a leader in the automotive aftermarket parts industry in the U.S. The company’s scale, unique distribution infrastructure, and customer service-oriented culture should allow it to take market share in a fragmented U.S. market for years to come.