Selective Opportunities in Japan’s Small-Cap Market

In the following commentary, the Portfolio Managers discuss the opportunities emerging in Japan’s small-cap market, highlighting improving corporate profitability, evolving management practices, and attractive valuations in a more selective market environment.

-

Takenari Okumura, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio Manager -

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Key Takeaways

» The second quarter stock market in Japan was defined by AI-driven enthusiasm and multiple expansion at the index level.

» With policy normalization, a gradual exit or consolidation of weaker companies should improve competition and benefit stronger, well-managed businesses over time.

» A primary concern of higher energy costs is a potential drag on personal consumption and will be watching for a softening in consumer sentiment in the second half of the year.

» Improving profitability and capital efficiency should support higher valuations for Japanese companies over time.

» While we remain mindful of growth deceleration and AI substitution risks, we continue to actively identify investment opportunities where we see credible paths to renewed growth at attractive entry points.

Would you please summarize the Japanese small-cap market in the second quarter of 2026?

The market advanced during the quarter, led by strong buying in artificial intelligence (AI) and semiconductor-related names, with the Tokyo Stock Index (TOPIX) reaching an all-time high in June. However, gains were narrowly concentrated in a handful of large-cap growth names, resulting in a pronounced bifurcation of the market. Small caps underperformed on a relative basis, pressured by rising interest rates and a rotation of investor capital into large caps. That said, stock-specific activity remained healthy, underpinned by expectations for domestic demand growth and ongoing corporate structural reforms. Overall, the quarter was defined by AI-driven enthusiasm and multiple expansion at the index level.

How did market volatility in 2Q26 affect your conviction in existing holdings, and where did it create opportunities to add, trim, or reassess positions?

During the quarter, we progressively trimmed positions in AI and semiconductor-related names where share price appreciation had materially narrowed the upside to our fair value estimates.

We redeployed that capital into two areas:

- Semiconductor-related names temporarily out offavor due to earnings softness despite attractivelong-term fundamentals

- Information technology (IT) and services nameswhere sentiment has turned overly pessimisticon concerns around AI substitution risk.

Which companies in the portfolio are direct and indirect beneficiaries of inbound tourism?

We believe direct beneficiaries are retailers with strong global brand recognition. Within our portfolio, we highlight Mizuno, which operates a globally recognized sporting goods brand and has been growing its inbound sales meaningfully, particularly in the sneaker category.

Among indirect beneficiaries, we point to Tanseisha, which specializes in the planning and design of hotels and commercial facilities. Renovation demand—driven both by the need to accommodate rising visitor volumes and by operators seeking to enhance customer appeal—continues to build steadily, and Tanseisha is well positioned to capture this trend.

As the Bank of Japan (BoJ) continues its gradual policy normalization, what effects are you seeing on smaller companies?

While the BOJ is proceeding with policy normalization, real interest rates remain negative and overall monetary conditions remain accommodative. With inflationary pressures stemming from Middle East tensions likely to feed through in the coming months, we expect the accommodative stance to persist, and view the drag from higher rates on the broader Japanese economy as limited.

If anything, we see the normalization process as a healthy development for small caps. The gradual exit or consolidation—through merger and acquisition (M&A) activity—of marginal small and micro-sized enterprises that had been sustained by the zero-interest-rate environment should improve the competitive dynamics of the domestic economy and benefit well-managed companies over time.

With geopolitical tensions contributing to volatility in global energy markets, how are higher energy costs affecting smaller companies in Japan?

A primary concern of higher energy costs is a potential drag on personal consumption. While wages continue to rise at a steady pace, the increases have not yet consistently outpaced price gains. Given the lag before cost increases are passed through to final goods, we are watchful of a possible softening in consumer sentiment in the second half of the year.

That said, a more encouraging structural shift is underway: Japanese companies—which have historically absorbed cost inflation through internal cost-cutting or margin compression—are increasingly willing to pass higher input costs through in a timely manner. Companies with strong pricing power tend to have durable customer relationships and high value-added offerings, and we expect a clear divergence in performance between those that can pass on prices and those that cannot.

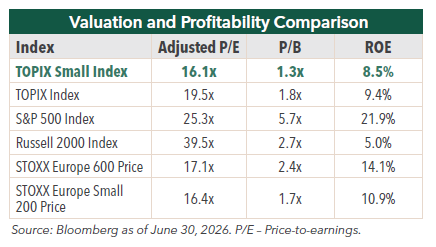

Following the recent strength in Japanese equities, where do you continue to see the most compelling valuation opportunities among domestically oriented small-cap companies?

We continue to see meaningful room for a price-to-book (P/B) re-rating driven by improving profitability.

One of the key reasons Japanese equities—and small caps in particular—trade at a discount to global peers is their historically low profitability. As Japanese companies sharpen their business portfolios through selection and concentration and address excess capital on their balance sheets, we expect return-on-equity (ROE) to trend higher, which in turn should support a re-rating of P/B multiples.

What is an example or two of a company that stands to benefit from rising wages and stronger domestic consumption in Japan?

One example is Transcosmos Inc., a leading player in Japan’s BPO (Business Process Outsourcing) industry, with a strong presence in call center operations. Rising wages are increasing corporate incentives to improve productivity, expanding demand for outsourcing non-core operations. The company is transitioning away from its historically fixed contract structures toward timely price revisions and performance-based pricing. Combined with scale benefits, this should drive meaningful margin expansion. Valuation stands at approximately 10x P/E and 1x P/B—levels that, in our view, do not reflect the company’s earnings growth potential, leaving meaningful upside.

Another example is United Arrows, which operates mid- to high-end select shops and is actively growing its private-label offering. Growth expectations had faded in prior years due to the prolonged absence of meaningful wage growth (which limited the company’s willingness to raise prices) and a slow pace of new store openings. Following a change in CEO, the company redefined its brand and, alongside the acceleration of wage growth, made the strategic decision to reposition both quality and price upward. This shift caught our attention and led us to initiate a position. If the company can break away from the “high quality at low prices” mindset common among Japanese firms, we see significant room for brand value enhancement. The inbound sales ratio currently sits at around 5% given the brand’s limited overseas recognition, but comparable Japanese apparel brands generate 30–40% of sales from inbound demand—suggesting a meaningful upside opportunity. Valuation is approximately 11x P/E and 1.6x P/B, which we do not believe fully reflects the company’s growth potential.

Looking ahead to the remainder of 2026, which domestic economic drivers are likely to be most important for the companies you own and why?

We believe the most important driver will be the ongoing shift in management mindset toward capital profitability.

Japanese companies have historically treated price pass-through as a last resort, preferring to manage through self-help cost reduction. However, the transition to a structurally inflationary environment—where increases in input costs and labor costs are persistent rather than transitory—is compelling companies to reassess this traditional approach.

While the small-cap universe is broad and company-specific circumstances vary widely, our bottom-up research confirms that management mindsets are evolving in a meaningful way. Since improving capital profitability directly translates into higher corporate value, we expect this structural shift to drive a re-rating of the small-cap segment over time.

What is your outlook for domestic Japanese companies for the remainder of 2026?

While easing Middle East tensions have driven oil prices lower, the pass-through to consumer prices typically occurs with a lag, and we remain mindful of near-term pressure on consumer sentiment from earlier price increases.

That said, the June Tankan survey, a widely followed measure of business confidence in Japan, points to improving corporate business sentiment, and we remain constructive on the outlook for the Japanese economy.

Within AI and semiconductor-related names, some stocks appear to already reflect near-term earnings expansion and pricing power in their valuations, and we are therefore taking a more selective stance in this area.

In IT and services, the correction that began with the “SaaS Is Dead” narrative has persisted, with some names now trading at P/E multiples in the low-teens—below the broader index. While we remain mindful of growth deceleration and AI substitution risks, we continue to actively identify investment opportunities where we see credible paths to renewed growth at attractive entry points.

- In this article:

- Japan

- Japan Small Cap Fund

You might also like

-

Investment Idea

Investment IdeaCompelling Valuations in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Masakazu Takeda, CFA, CMAPortfolio Manager Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment Idea

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaJapanese equities are currently trading at compelling valuation levels compared to other developed equity markets around the world and relative to their own historical averages. We believe the Japanese market deserves a closer look.

-

Investment Idea

Investment IdeaWhy Active Matters When Investing in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaWhen investing in Japanese businesses, we believe it is imperative to select a manager who is immersed in the culture and can perform in-depth, company-specific research to build a concentrated portfolio of Japanese companies that can outperform a benchmark and weather volatility.

-

Company Spotlight

Company Spotlight

Japan FundBerkshire Hathaway’s Stake in Tokio Marine Highlights the Appeal of Japanese Insurers

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio ManagerRead the SpotlightTokio Marine is Japan’s largest general insurance group with a solid track record in the domestic market and an expanding overseas business. Tokio Marine is one of three Japanese insurers that has significant market share and enjoys high profitability and strong pricing power due to industry consolidation—qualities Berkshire Hathaway appears to have noticed.