Identifying Select Opportunities in Japanese Businesses

In the following commentary, the Portfolio Managers discuss Japan’s improving corporate fundamentals, the continued benefits of governance reform, and why stock selection remains essential as the market becomes increasingly differentiated.

-

Masakazu Takeda, CFA, CMAPortfolio Manager

Masakazu Takeda, CFA, CMAPortfolio Manager -

Angus Lee, CFAPortfolio Manager

Angus Lee, CFAPortfolio Manager

Key Takeaways

» With a transition to modest inflation and gradually rising interest rates in Japan, companies are placing greater emphasis on capital efficiency, ROE, and balance sheet discipline.

» Rather than focus on short-term currency movements, we focus more on companies with pricing power, global revenue streams, and durable cost structures that can support long-term competitiveness.

» AI infrastructure investment is creating new opportunities for Japanese companies, particularly in semiconductor equipment, electronic components, and precision manufacturing.

» Our interest in housing-related businesses is based on the long-term fundamentals of the U.S. housing market. We view the combination of structural supply-demand support, market-share expansion potential, and attractive valuations as a compelling long-term investment opportunity.

» Our outlook for Japan remains constructive; we believe in today’s environment, stock selection is particularly important where market prices do not fully reflect intrinsic value.

Would you please summarize the strong year-to-date Japanese market?

Japanese equities have performed strongly year-to-date, but the underlying picture is more nuanced than the headline indices suggest.

Performance has been driven in part by artificial intelligence (AI) and semiconductor-related names, supported by global demand and developments in U.S. technology markets. At the same time, returns have been more mixed across other areas of the market, with parts of the small- and mid-cap universe and certain export-oriented sectors lagging.

As a result, returns have been somewhat concentrated, and dispersion remains meaningful. In this environment, we continue to see opportunities at the individual stock level where valuations do not fully reflect underlying fundamentals.

How is corporate Japan adapting to higher interest rates?

Japan’s transition toward modest inflation and gradually rising interest rates represents a structural normalization rather than a source of instability.

In this context, corporate behavior is evolving. Companies are placing greater emphasis on capital efficiency, return on equity (ROE), and balance sheet discipline, alongside a more proactive approach to shareholder returns.

In our view, this reflects the ongoing progress of corporate governance reform and is becoming increasingly visible in practice.

With geopolitical tensions contributing to volatility in global energy markets, how are higher energy costs affecting Japanese consumers and companies?

The impact of higher energy costs has been felt primarily through the inflation channel. Rising energy prices have contributed to upward pressure on the consumer price index (CPI). While wages are increasing, the pace of improvement in real wages remains gradual, which has led to continued caution in consumer spending.

From a corporate perspective, the impact has been more indirect. Companies are navigating higher input costs through pricing and efficiency measures. At this stage, the effect is better understood as a moderating factor on demand, rather than a broad deterioration in corporate fundamentals.

How do you think about currency risk when investing in Japan?

We do not base investment decisions on short-term currency movements. While currency fluctuations can affect reported earnings, they do not change the underlying intrinsic value of a business.

What matters more is whether a company has pricing power, a globally diversified revenue base, and a cost structure that allows it to operate effectively across different environments. Many leading Japanese companies have evolved in this direction.

As a result, their long-term competitiveness is less dependent on exchange rate movements than in the past.

How has U.S. technology spending influenced opportunities across the Japanese equity market?

Global investment in AI infrastructure, particularly in the U.S., has been an important driver of opportunities for Japanese companies. Japan plays a critical role in areas such as semiconductor manufacturing equipment, electronic components, and precision manufacturing.

At the same time, we would note that investor attention has become highly concentrated on a limited group of visible AI beneficiaries. In some cases, valuations appear to reflect optimistic expectations for several years ahead.

While the structural opportunity remains compelling, we believe it is important to approach this area with selectivity, and to recognize that value creation will not be evenly distributed across the sector.

Would you please discuss the long-term fundamentals of the U.S. housing market and your investment thesis for the Fund’s housing-related holdings?

Our interest in housing-related businesses is based on the long-term fundamentals of the U.S. housing market. The U.S. continues to face a structural shortage of single-family homes, driven by sustained household formation and a prolonged period of under-supply following the global financial crisis. Berkshire Hathaway’s increased exposure to housing-related businesses reinforces the view that, despite near-term headwinds from elevated mortgage rates, the long-term opportunity remains intact.

Against this backdrop, Japanese homebuilders such as Sekisui House, Sumitomo Forestry, and Daiwa House have been steadily expanding their presence in the U.S. through acquisitions and operational improvements. In our view, the opportunity extends beyond a cyclical recovery in U.S. housing demand. The key investment thesis is that these companies can gradually gain market share by leveraging strengths in construction efficiency, prefabrication and manufacturing processes, housing quality, and financial resources that many local competitors do not possess.

Recent acquisitions, including Sekisui House’s purchase of M.D.C. Holdings and Sumitomo Forestry’s acquisition of Tri Pointe Homes, demonstrate the commitment of Japanese builders to the U.S. market. At the same time, the sector remains largely overlooked by investors, with many companies trading at undemanding valuations despite solid profitability and attractive dividend yields. While the timing of a housing recovery remains uncertain, we view the combination of structural supply-demand support, market-share expansion potential, and attractive valuations as a compelling long-term investment opportunity.

Which investment thesis within the portfolio has strengthened the most so far in 2026?

The theme that has continued to strengthen is the improvement in corporate behavior driven by governance reform. This is visible in a greater focus on profitability and ROE, more active capital allocation decisions, and an increasing willingness to return capital to shareholders.

At a broader level, this is supported by Japan’s transition away from deflation. Together, these factors are contributing to a structural improvement in the quality and valuation of Japanese companies over time. In our view, this remains one of the most important structural drivers for Japanese equities.

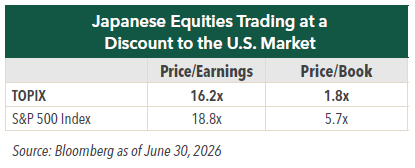

As we head into 3Q26, how do equity valuations look in Japan vs. the U.S.?

Even after the recent rally, Japanese equities continue to trade at a discount to the U.S. market. This is notable given that corporate profitability has improved and structural reforms continue to progress.

In our view, this combination—improving fundamentals alongside relatively modest valuations—remains an attractive and distinguishing feature of the Japanese equity market.

What is your outlook for the Japanese market over the remaining six months of 2026?

The overall environment remains constructive, supported by ongoing corporate governance reform, gradual economic normalization, and Japan’s role in global industrial and technological supply chains.

At the same time, the market has become increasingly differentiated. Investor attention has been concentrated in certain sectors, while other areas remain underappreciated. In this environment, we believe returns will be driven less by overall market direction and more by individual stock selection, particularly where there is a meaningful gap between market price and intrinsic value.

As always, our approach remains unchanged: to invest in high-quality businesses with strong management at attractive valuations, and to allow time for that value to be realized.

- In this article:

- Japan

- Japan Fund

You might also like

-

Investment Idea

Investment IdeaCompelling Valuations in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager Tadahiro Fujimura, CFA, CMAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager Takenari Okumura, CMAPortfolio ManagerRead the Investment Idea

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaJapanese equities are currently trading at compelling valuation levels compared to other developed equity markets around the world and relative to their own historical averages. We believe the Japanese market deserves a closer look.

-

Investment Idea

Investment IdeaWhy Active Matters When Investing in Japan

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio Manager

Tadahiro Fujimura, CFA, CMAPortfolio Manager

Takenari Okumura, CMAPortfolio ManagerRead the Investment IdeaWhen investing in Japanese businesses, we believe it is imperative to select a manager who is immersed in the culture and can perform in-depth, company-specific research to build a concentrated portfolio of Japanese companies that can outperform a benchmark and weather volatility.

-

Company Spotlight

Company Spotlight

Japan FundBerkshire Hathaway’s Stake in Tokio Marine Highlights the Appeal of Japanese Insurers

Masakazu Takeda, CFA, CMAPortfolio Manager

Angus Lee, CFAPortfolio ManagerRead the SpotlightTokio Marine is Japan’s largest general insurance group with a solid track record in the domestic market and an expanding overseas business. Tokio Marine is one of three Japanese insurers that has significant market share and enjoys high profitability and strong pricing power due to industry consolidation—qualities Berkshire Hathaway appears to have noticed.