Meeting America’s Growing Energy Needs with Natural Gas

The Portfolio Managers discuss the drivers behind the Fund’s outperformance, the industry’s long-term growth outlook, and why utilities remain attractively valued.

-

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager -

L. Joshua Wein, CAIAPortfolio Manager

L. Joshua Wein, CAIAPortfolio Manager

Key Takeaways

» The Fund’s energy infrastructure allocation provided a meaningful boost to 2026 performance.

» The U.S. natural gas industry continues to demonstrate its essential role in meeting periods of elevated energy demand, whether by extreme weather, geopolitical events, or the growing need for reliable power generation.

» Stronger-than-average projected earnings growth is being driven primarily by rising demand for electricity.

» Utilities are positioned to benefit from rising long-term electricity demand.

» We view the valuations of utilities as attractive due to their current valuations and their above-average projected growth.

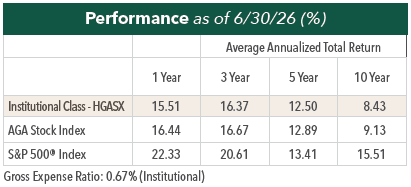

Would you please summarize the performance of utilities and the Fund in 2026?

Utilities overall have slightly outperformed the overall market in 2026, with multi-utilities and electric utilities leading the sector. While the overall market experienced significant volatility, including a sharp selloff during the early stages of the Iran conflict followed by a strong recovery, utilities delivered much steadier performance, as has historically been the case.

The Hennessy Gas Utility Fund has also performed well this year, outperforming utilities and the S&P 500® Index. While the Fund has benefited from the solid performance of utility companies, a meaningful contributor has been its exposure to energy infrastructure. The conflict in Iran contributed to higher oil prices, which supported the performance of energy-related holdings.

Although the Fund is primarily invested in utilities, it also has exposure to other areas of the energy value chain through major pipeline companies that transport both natural gas and crude oil throughout North America. These holdings have provided an additional tailwind to relative performance this year.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting hennessyfunds.com.

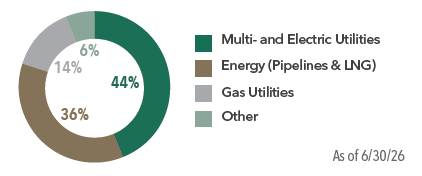

Would you please describe the current breakdown of the Fund?

The Fund is generally divided into three segments: 44% in multi- and electric utilities, 36% in energy infrastructure, and 14% in natural gas utilities. The energy infrastructure allocation consists primarily of major pipeline companies that transport crude oil and natural gas throughout North America as well as a single pure-play LNG export company, Cheniere Energy.

While many of the holdings have some exposure to LNG exports or benefit from delivering natural gas to liquefaction facilities, LNG remains a relatively small driver of overall Fund performance.

In addition, the Fund does not invest in exploration and production (E&P) companies. As a result, the price of natural gas itself is generally not a primary driver of performance. Instead, the Fund is more closely tied to growing demand for natural gas and the volumes transported through the nation’s energy infrastructure.

What is driving the above-average projected earnings per share (EPS) growth for utilities?

Stronger-than-average projected earnings growth is being driven primarily by rising demand for electricity. Key drivers include the expansion of data centers and AI infrastructure, the onshoring of manufacturing, and increasing energy needs across the industrial and commercial sectors. Meeting this demand will require significant investment in generation, transmission, and distribution infrastructure, creating a favorable environment for regulated utility earnings growth over the coming years.

We also believe the regulatory environment remains constructive, with allowed returns on equity generally remaining consistent with historical levels and supporting continued investment in utility infrastructure.

How are natural gas utilities preparing to meet growing demand from data centers, AI infrastructure, and power generation?

We believe natural gas utilities, and utilities in general, have a significant opportunity as growing electricity demand from data centers, AI infrastructure and the onshoring of manufacturing drives the need for additional power generation over the next decade and beyond. Most companies are taking a prudent, measured approach to this potential growth, and opportunities vary by region. Also, these projects generally take longer to develop than many investors expect.

That said, the long-term growth outlook for these companies is vastly stronger than it was five years ago, when many investors questioned whether natural gas would simply serve as a transition fuel on the path to a fully renewable energy system. Today, the conversation has shifted. Rather than debating terminal values, investors are increasingly focused on how quickly growth can accelerate and how long that growth can be sustained.

What are the biggest opportunities and constraints facing the U.S. natural gas industry over the next several years?

The U.S. natural gas industry continues to demonstrate its essential role in meeting periods of elevated energy demand, whether by extreme weather, geopolitical events, or the growing need for reliable power generation. These themes were reinforced at this year’s American Gas Association (AGA) Financial Forum, where industry leaders emphasized the increasingly important role natural gas plays in providing reliable, affordable energy.

Natural gas production, consumption, and exports continue to hit all-time highs and are projected to keep growing. With over 100 years of natural gas supply, the U.S. is well positioned to meet its own demands while remaining the world’s largest exporter. This abundant domestic resource base has also allowed U.S. natural gas prices to remain significantly lower and less volatile than those in Europe and Asia, providing an important competitive advantage for both consumers and manufacturers.

Potential constraints include infrastructure bottlenecks, such as insufficient pipeline capacity or LNG export facilities and vessels, as well as the possibility that AI-related investment and data center construction develop more slowly than currently anticipated, reducing future demand growth.

How do Utilities’ valuations compare to the overall market currently and historically?

As of the end of the quarter, Utilities were trading at about a 15% discount to the S&P 500 on a forward price-to-earnings (P/E) basis, which is historically below trend. In addition, Utilities were trading at a slight discount to their own historical average P/E as of the end of June 2026.

We view the valuations of utilities as attractive, despite the better relative performance this year, due to both their current valuations but also their above-average projected growth.

- In this article:

- Energy

- Gas Utility Fund

You might also like

-

Investment Idea

Investment IdeaDefining the Energy "Value Chain"

Ben Cook, CFAPortfolio ManagerRead the Investment Idea

Ben Cook, CFAPortfolio ManagerRead the Investment IdeaEnergy is a large and complex sector. The sector’s broad sub-industries can be divided into a “value chain,” each segment of which has different characteristics and offers different investment opportunities.

-

Fund Commentary

Fund Commentary

Energy Transition FundEnergy Resilience and a Changing Power Landscape

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, Portfolio Managers Ben Cook and Josh Wein discuss energy sector performance, continued capital discipline, recent mergers and initial public offerings (IPOs) and valuations.

-

Fund Commentary

Fund Commentary

Midstream FundMidstream Companies’ Role in the Energy Buildout

Ben Cook, CFAPortfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryPortfolio Managers Ben Cook and Josh Wein discuss the midstream sector’s strong first-half performance, rising natural gas infrastructure demand, the sector’s prudent capital allocation, and what we believe to be attractive valuations.